What do you call an accountant with specialized auditing and investigative skills? A forensic accountant who can help resolve disputes involving fraud and testify as an expert witness in a courtroom battle.

In an age where securities fraud, shareholder disputes, employee theft, insurance fraud, personal injury claims, and other criminal investigations are running rampant, forensic accountants are not just useful – they’re essential in the business world.

Here are just a few of the tasks that forensic accountants

undertake for clients:

Investigate and analyze financial evidence to detect employee theft.

Conduct business investigations that involve funds tracing, asset identification and recovery.

Detect fraud in financial statements through forgery, collusion, missing documents and other factors.

Develop computer programs to help analyze and present evidence in court.

Issue reports, exhibits and collections of documents to assist in legal proceedings.

Contact our office to learn more about forensic accounting.

You may see it on a TV crime show, but this is a specialty that can also help

your company in the real world.

So-called “pass-through” entities — including partnerships, limited liability companies (LLCs) and S corporations — generally aren’t required to pay entity-level taxes. So, when it comes to valuing a small business structured as a pass-through entity for tax purposes, people often wonder: Would investors pay a premium for an interest in this business compared to an interest in an otherwise identical C corporation? And, if so, how much is this favorable tax treatment worth? This is the crux of the tax-affecting debate.

Much of the litigation regarding this issue comes from the IRS and tax courts. But a recent Tennessee Court of Appeals decision discusses this issue in the context of a shareholder buyout. (Raley v. Brinkman, No. 2018-02002, Tenn. App., July 30, 2020)

Pros and Cons of Pass-Throughs

For pass-through entities, all items of income, loss, deduction and credit pass through to the owners’ individual tax returns, and taxes are paid at the personal level. Distributions to owners generally aren’t taxable to the extent that owners have positive tax basis in the entity.

If a pass-through entity distributes just enough of its earnings to cover the owners’ tax liabilities, there may be little potential valuation difference at the investor level between the pass-through entity and a taxable entity, assuming similar tax rates at the entity and the investor levels. If the pass-through entity distributes larger amounts of earnings to the owner, the interest becomes potentially more valuable than an equal interest in a taxable entity, all other things being equal. If the pass-through entity distributes less than the tax liability amount, an interest in the taxable entity could potentially be more valuable in the hands of the owner.

Court Allows Tax Affecting

The tax-affecting issue took center stage in a recent buyout case involving two equal partners in a restaurant that generated roughly $3.4 million in gross annual income in 2016. When the owners disagreed about how to manage their business, a Tennessee trial court ordered a buyout of one owner’s interest at “fair value” under applicable state law.

The business operated as an LLC that elected to be treated as an S corporation for income tax purposes. The trial court allowed the buyout price to include a hypothetical 38% corporate income tax rate to the restaurant’s earnings. But the seller (plaintiff) appealed, arguing that tax affecting wasn’t appropriate for a pass-through business that wasn’t subject to entity-level tax.

The buyer (defendant) contended that tax affecting was appropriate because the income from an S corporation passes through to the owners’ individual tax returns and is taxed at the owners’ personal tax rates. He also argued that valuation experts commonly use after-tax income values to calculate the capitalization rate under the income approach.

The appellate court explained that the problem with using the income approach to value a pass-through entity is that it’s designed to discount cash flows of C corporations, which are taxed at both the entity and the shareholder level. Income from an S corporation is taxed only at the shareholders’ personal level.

Citing the landmark Delaware Open MRI Radiology Associates case, the appellate court concluded that declining to tax affect an S corporation’s earnings would overvalue it, but charging the full corporate rate would undervalue it by failing to recognize the tax advantages of S status. The court also determined that it was appropriate to use an after-tax earnings stream because the expert’s capitalization rate was based on after-tax values.

Finally, the appellate court cited the Estate of Jones. In this U.S. Tax Court case, the court concluded that the cash flows and discount rate should be treated consistently when valuing a pass-through entity.

IRS Job Aid Provides Insight

The debate over tax affecting pass-through entities has persisted for decades. To help clarify matters, the IRS has published a job aid entitled “Valuation of Non-Controlling Interests in Business Entities Electing To Be Treated As S Corporations for Federal Tax Purposes.” This document helps IRS valuation analysts evaluate appraisals of minority interests in S corporations for federal tax purposes.

However, the job aid provides useful guidance on the issue of tax affecting that may be applied more generally to all types of pass-through entities that are appraised for any purposes, not just for tax reasons. Business valuation experts may use this job aid as a reference tool to help support their decisions to apply tax rates to the earnings of pass-through entities when projecting future cash flows.

No Bright-Line Rules

When it comes to tax affecting pass-through entities, there’s no clear-cut guidance that prescribes a specific tax rate — or denies tax affecting altogether. Rather, tax affecting may be permitted on a case-by-case basis, depending on the facts and circumstances.

Business brokers say fear of a recession and uncertainty over the upcoming presidential election may be driving down business valuations, according to the third-quarter edition of Market Pulse, the quarterly survey of business brokers conducted by the International Business Brokers Association and M&A Source.

Fifty-three percent of business brokers surveyed cited the prospect of a recession as the biggest concern affecting U.S. business valuations, followed by the presidential election and the trade war with China.

“Small business owners are worried that a recession is coming, and trade issues are causing volatility. All that nervous energy means buyers are dialing back a bit – particularly on the smaller market deals.” said Craig Everett, PhD. Everett is director of the Pepperdine Capital Markets Project at the Pepperdine Graziado Business School, which compiled the survey results.

The national survey is intended to capture market conditions for businesses sold for less than $50 million. It divides that market into three classes of main street businesses with values of $2 million or less, and two lower middle-market ones in the $2 million to $50 million range.

The survey found that businesses selling for $5 million to $50 million garnered a 9 percent premium over asking price during the third quarter, while the smallest main street businesses, those worth less than $500,000, sold for just 85 percent of asking price, the lowest percentage in four years.

Scott Bushkie, managing partner of Cornerstone Business Services, told Market Pulse that falling business confidence has slowed the activity of the individual buyers who account for most main street business acquisitions.

“Confidence always gets shaky as we enter an election season,” said Bushkie, whose firm has an office in Iowa, where the first caucus of the 2020 presidential campaign will be held February 3. “There’s this general escalation of reports pointing out economic weaknesses and policy flaws, and people sometimes internalize that negativity. I think we may be feeling that even earlier than normal this time around.”

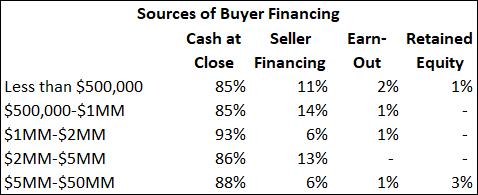

Seller financing

Market Pulse found that sellers provided roughly 10 percent of the buyer’s financing in deals that closed during the third quarter. Earn-outs and retained equity were less common.

“Lenders always like to see sellers keep some skin in the game,” said Justin Sandridge of Murphy Business Sales-Baltimore East. “When sellers aren’t willing to finance any of the purchase price, that sends warning signals to buyers and lenders alike. Refusing to provide seller financing is like holding up a giant ‘no confidence’ sign, and it’s likely to scare other parties away from the deal.”

Market Pulse’s third-quarter survey of 236 business brokers and M&A advisors was conducted from October 1-15. The respondents reported completing 210 transactions during the third quarter.

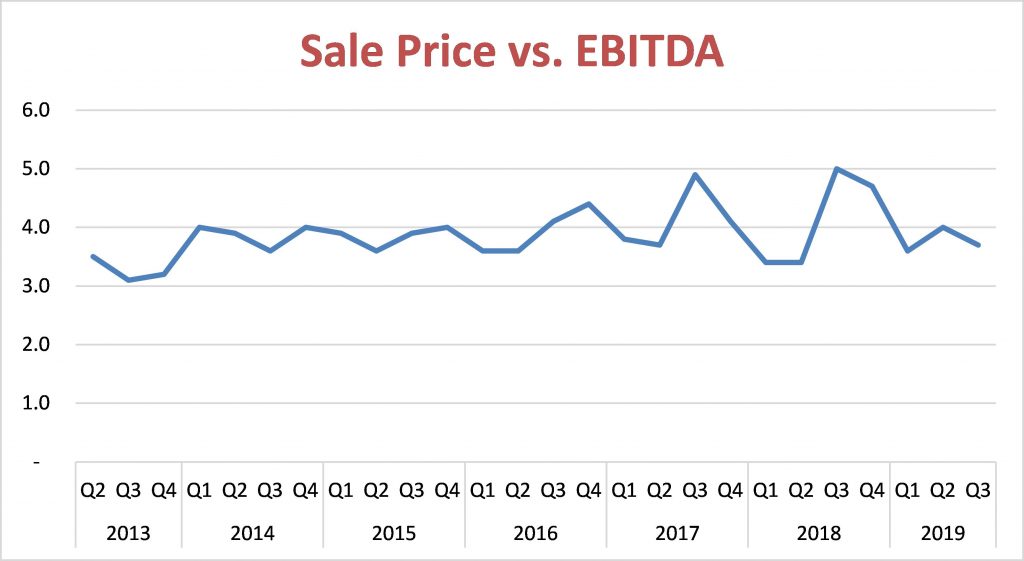

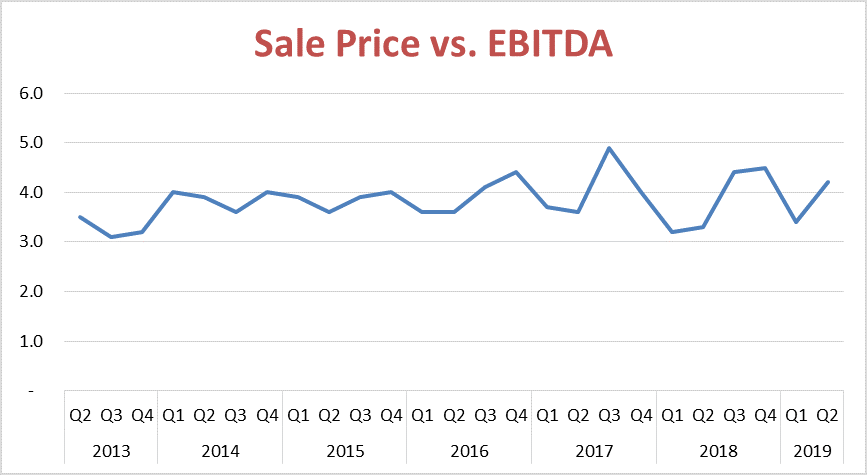

Small business sales during the third quarter of 2019 yielded EBITDA multiples about 26 percent lower than a year before, according to the latest edition of DealStats Value Index. It’s one of several developments noted in the report that point to an emerging buyer’s market.

The median EBITDA multiple – the ratio of selling price to earnings before interest, taxes, depreciation and amortization – slid to 3.7 for transactions completed in the third quarter, down from 4.0 during the preceding quarter and the peak of 5.0 reached during the third quarter of 2018. The EBITDA multiple during the third-quarter of 2018 was the highest quarterly mark since at least 2013.

DealStats is a database of private-company transactions maintained by Business Valuation Resources. The database is used by business appraisers when applying the market approach to valuation. Multiples such as sale price-to-EBITDA can be derived from transactions involving similar businesses and used to estimate the value of a company, subject to adjustments for unique characteristics of the business being valued.

Over the longer term, DealStats notes that EBITDA multiples have generally trended downward since 2017, falling to a six-year low in 2019.

It’s important to bear in mind that DealStats data only reflects transactions reported to the service, and the data is subject to revision as additional sales are reported. For instance, the median EBITDA multiple for the April-June quarter was initially reported as 4.2. That was revised to 4.0 in the latest report. The spike to 5.0 during the third quarter of 2018 was previously reported as 4.4 and 4.5.

The delays in reporting may limit the value of information regarding trends gleaned from the quarter-to-quarter gyrations of multiples.

EBITDA margins decline

Businesses sold in 2019 have tended to be less profitable than those sold in recent years, according to the DealStats data. The median EBITDA margin (measured as a percentage of revenue) was just below 11 percent during the third quarter, up slightly from the second quarter, but down from 12 percent in the first three months of the year. EBITDA margins have generally trended lower since 2013.

A long time to sell

Businesses are taking longer to sell, according to DealStats. The median number of days for private businesses to sell was 221 for deals closed during the first half of 2019. That marked the fifth straight half-year period (dating back to the first half of 2017) where the median exceeded 200. From 2013 to 2016, the median never topped 200 days.

Revenue multiple falls

DealStats reports that the median sale price-to-revenue multiple this year is 0.45, down from 0.49 in 2018 and the lowest multiple in at least a decade. Businesses in the finance/insurance sector garnered the highest multiple, at 1.75, followed by information at 1.70 and professional, scientific and technical services at 0.89.

The highest EBITDA multiple was noted in the information sector, at 11.1, followed by mining, quarrying and oil and gas extraction, at 8.5. The lowest multiple was 2.6 for the accommodation and food service industry.

Business valuation professionals use transactions such as those collected by DealStats to derive a business’s market value. If you have questions about how comparable sales influence the value of your business, or how much your business is worth, please contact us.

WeWork has accepted a bailout by its largest investor, SoftBank Group, which will take an 80 percent ownership stake in the company, according to multiple media reports. The rescue package reportedly values the company at about $8 billion, a stunning reversal from its $47 billion valuation in January, based on SoftBank’s infusion of $6 billion at the time.

From a valuation perspective, the rapid deflation of WeWork’s bubble speaks to the hazards of investing in unproven young companies. This year has seen a string of high-profile initial public offerings by companies that don’t make money (most notably Uber and Lyft) and face stern questions about their paths to profitability. Uber in particular has been growing revenue at the expense of profit, while creating unrealistic customer expectations about the actual cost of transportation – or of having a hamburger and fries delivered to your home.

WeWork was built on a similar model, although its results have been even more extreme. The company, which leases office buildings, spends millions sprucing them up, then subdivides them and seeks to fill them with member/lessees, loses more than $5,000 per customer, according to its public filings. The company lost $690 million during the first half of 2019 on $1.5 billion in revenue. Last year, it lost $1.6 billion on revenue of $1.8 billion.

In January, it was valued at $47 billion, or 26 times its 2018 revenue, based on the SoftBank investment. That multiple, it turns out, was too rich for investors. The company’s IPO filing in August inspired a wave of intense scrutiny and criticism, culminating in the withdrawal of the IPO on September 30.

The failed IPO is a reminder that investing in young, money-losing companies marries the prospect of lofty rewards with a high failure rate. As MarketWatch columnist Brett Arends pointed out in his excellent recent piece on Uber, the experts frequently make mistakes in valuing “revolutionary” companies. He notes that powerhouses like Amazon, Facebook and Netflix all faced questions early on about untested management, potential strategic missteps and supposedly rich valuations.

Unlike those companies, WeWork has yet to articulate how it might ever achieve profitability. An early hint regarding the company’s fate came in 2017, when founder and then-CEO Adam Neumann told Forbes, “Our valuation and size today are much more based on our energy and spirituality than it is on a multiple of revenue.”

While it’s important to do your homework before making any investment, betting on an unprofitable young company requires a leap of faith. Unlike Neumann, who will reportedly receive more than a billion dollars to walk away, the rest of us don’t get parachutes.

Divorce is almost always complicated, especially when there is a lot at stake. In today’s article, we will explore the handling of stock compensation in divorce proceedings.

Compensation for executives in medium and large corporations often goes beyond standard payroll and perquisites (the special rights that come with the position). It can also include forms of payment to reward the executive for prior performance or to encourage strong future performance. This compensation can take the form of stock options or restricted stock units (RSUs).

In New York (an equitable distribution state for purposes of dividing marital assets) stock options and RSUs acquired during the marriage are presumed to be marital property, unless the holder can prove they were acquired as a gift or inheritance or in exchange for other non-marital property. One can determine if the options were granted as a reward for past services by examining the plan documents, such as the Stock Options Plan and the Options Statement. These documents should address exercise price, expiration date and other terms, including some that may pertain to divorce.

If the stock is publicly traded, its value is based on the fair market value of the stock – the amount at which a share of stock is being traded – usually at the date of trial or the date of the legal action. Valuation of the stock of a privately held company is more problematic, and will necessitate a business valuation. When performing the business valuation, the appraiser examines a host of factors, including the type of business, prior sales of company stock, the future outlook for the company and goodwill.

The non-propertied spouse must be watchful for deception, particularly in smaller companies, where the executive can negotiate, sometimes orchestrate, their compensation package. In other words, were the stock options granted as a reward in addition to normal compensation? Or is the executive receiving the options in lieu of a raise?

The New Jersey Appellate Court recently decided a case regarding how RSU compensation should be evaluated and divided in a divorce. In M.G. v. S.M., the plaintiff’s employer had issued RSUs to the plaintiff over the course of an eight-year period. These RSUs were subject to a vesting schedule established by the employer. After a stated period of time, vesting would occur and the employee would take ownership of the stock.

Although eight years’ worth of RSUs had been granted to the plaintiff, at the time of the filing of the divorce complaint, only three years of the grants were vested. At trial, the judge heard testimony from the plaintiff about the stock units, including the plaintiff’s agreement that the defendant was entitled to share in the value of the vested units.

However, the plaintiff argued that the non-vested RSUs were not distributable to the defendant. The plaintiff submitted evidence that his company issued the RSUs to employees to incentivize future performance and encourage them to remain with the company so that their interests in the RSUs would vest. The trial court’s opinion was that all of the RSUs were “the result of prefiling, marital efforts, and are thus subject to equitable distribution,” regardless of when they vest.

There is a lack of significant guidance in the form of case law with respect to how RSUs are divided in divorce in many states. The Appellate Court explored the possible methods by which to value and divide the assets. The court ultimately deciding to rely on guidance from a Massachusetts case that dealt with the same subject. The New Jersey Appellate Court held that the following is the appropriate analysis to consider when dividing RSUs in a divorce:

Where a stock award has been made during the marriage and vests prior to the date of complaint, it is subject to equitable distribution.

Where an award is made during the marriage for work performed during the marriage, but becomes vested after the date of the complaint, it, too, is subject to equitable distribution.

Where the award is made during the marriage, but vests following the date of complaint, there is a rebuttable presumption that the award is subject to equitable distribution, unless there is a material dispute of fact regarding whether some or all of the award was consideration for future performance.

The Appellate Court went on to state that the party who wants to exclude the assets – i.e. the party to whom the RSUs were granted – must demonstrate that they were issued for work performance after the filing of the complaint for divorce.

Based on the Appellate Court’s decision, it is likely that the plaintiff in M.G. v. S.M. will be successful in excluding at least a portion of the unvested RSUs from equitable distribution of the marital estate, as his trial testimony stated that his employer’s intent in issuing RSUs was to encourage positive future performance.

Therefore, the purpose for which the executive compensation is issued by the employer may also impact the division of those assets in divorce. If you have questions about how your executive compensation package may be valued, contact Advent Valuation Advisors today.

The case is Superior Court of New Jersey Appellate Division Docket No. A-1290-17t1, December 26, 2018. The decision is available here:

The Tax Court recently issued a ruling that addresses the tax-affecting of pass-through entity earnings in valuing a portion of the entity. The case, Estate of Aaron Jones v. Commissioner, involved valuing interests in pass-through entities engaged in the lumber industry for the purpose of determining gift tax.

In valuing the taxpayer’s interest in the companies, the taxpayer’s valuation expert tax-affected projected earnings by 38 percent, because the valuation in question was as of 2009. He then applied a 22 percent premium for holding pass-through entity tax status because of the benefit of avoiding the dividend tax.

The IRS argued that there should be no tax imputed because (a) there is no tax at the entity level, (b) there is no evidence that the entity would become a taxable C corporation, and (c) tax-affecting abandons the arm’s-length formulation of fair market value, “in the absence of a showing that two unrelated parties dealing at arm’s length would tax-affect” the interest’s earnings “because it inappropriately favors a hypothetical buyer over the hypothetical seller.”

The estate’s expert argued that a tax rate of zero would overstate the value of the interest, because the partners are taxed at their ordinary rates on partnership income whether or not the company distributes any cash, and a hypothetical buyer would take this into consideration. He also argued that the hypothetical buyer and seller would take into account the benefit of avoiding dividend taxes.

Interestingly, the court noted that while the IRS “objects vociferously” to the estate expert’s tax-affecting of income, the IRS’ experts were silent on the matter. “They do not offer any defense of respondent’s proposed zero tax rate. Thus, we do not have a fight between valuation experts but a fight between lawyers.”

An emerging path

Taxpayers – and the valuation community – have been fighting the IRS over this issue for years, starting with Gross v. Commissioner in 1999 (TCM 1999-254), which rejected the use of tax-affecting when valuing pass-through entities. Courts have generally sided with the IRS in opposing the tax-affecting of pass-through entities in subsequent cases such as Estate of Gallagher v. Commissioner in 2011 (TCM 2011-148).

Jones is the second notable decision this year in which a court has supported the use of tax-affecting in valuing pass-through entities in cases where additional adjustments were made to address the economic benefits of such entities. The other case, Kress v. United States, was decided in March by the District Court for the Eastern District of Wisconsin (16-C-795). There, as in Jones, the court’s decision relied heavily on the taxpayer’s expert.

In Jones, the court went back to the Gross case, quoting from Gross that “the principal benefit that shareholders expect from an S corporation election is a reduction in the total tax burden imposed on the enterprise. The owners expect to save money, and we see no reason why that savings ought to be ignored as a matter of course in valuing the S corporation.”

The court also referenced Gallagher and Estate of Giustina v Commissioner (TCM 2011-141), stating that all three cases did not question the efficacy of taking into account the pass-through tax status, but rather how to do so.

The court credited the estate’s expert for recognizing both the immediate tax burden posed by a pass-through entity’s income, and the benefit of avoiding the dividend tax. The “tax-affecting may not be exact, but it is more complete and more convincing than respondent’s zero tax rate.”

The case is Estate of Aaron Jones v. Commissioner, TCM 2019-101, Docket No. 27952-13, filed August 19, 2019. See pages 36-42 for pertinent details.

Business brokers say the U.S.’s ongoing tariff battles are taking a bite out of business transactions.

Concerns over the impact of tariffs have compelled some small-business owners to lower their asking prices, while others have chosen not to put their businesses on the market at all, according to the second-quarter edition of Market Pulse, the quarterly survey of business brokers conducted by the International Business Brokers Association and M&A Source.

During the second quarter, 32 percent of lower middle market advisors and 22 percent of “Main Street” advisors reported that one or more of their sellers had been affected by tariff issues, according to Market Pulse. Main Street businesses are defined as those with values of $2 million or less, and lower middle-market ones as those worth $2 million to $50 million.

The brokers reported that some of the affected buyers had reduced their asking prices because of tariff-related concerns, while others decided not to sell as a result of recent changes in trade policy with China, Mexico and Canada, according to the report. Brokers say the timing couldn’t be worse for business owners looking to cash out during what has been a strong seller’s market.

“What’s tragic is that M&A conditions are otherwise extremely strong for sellers right now. However, there is a substantial minority of small business owners affected by tariff issues who can’t take full advantage of this market to exit their business,” Laura Maver Ward, managing partner of Kingsbridge Capital Partners, told Market Pulse. “Many business owners would rather lower their purchase price – reducing their retirement resources and their reward for years of hard work – rather than take a chance on missing their window to sell their company.”

The Market Pulse report echoes findings of a survey conducted early this year by the National Federation of Independent Business. In that survey, 37 percent of small business owners reported negative impacts of U.S. trade policy changes with Mexico, Canada and China.

Manufacturers hit hard

Several brokers cited in the Market Pulse report said that manufacturing clients have been among those hardest hit by tariffs. While the pace of manufacturing deals has been hampered, activity in the construction/engineering sector has heated up, driven in part by private-equity interest, according to the report.

Market Pulse reported that overall market sentiment fell during the second quarter across all five value ranges tracked in the survey, when compared to confidence levels a year before. That said, 66 percent or more of advisors still see a seller’s markets in each of the three value ranges between $1 million and $50 million. Sentiment in the two value ranges below $1 million are at or below 50 percent.

“It’s still a strong marketplace with more buyers than sellers, and companies, for the most part, are doing well,” Randy Bring of Transworld Business Advisors told Market Pulse. “But tariff issues are popping up, and talk of a recession in the next 12 to 18 months is scaring some buyers away.”

Market Pulse is compiled by the Pepperdine Private Capital Markets Project at Pepperdine Graziadio Business School. To learn more, go to Pepperdine’s Market Pulse page:

The former operator of a medical taxi service in Orange County was sentenced Thursday to one to three years in prison for defrauding Medicaid of more than $200,000. Photo by Bill Oxford on Unsplash

The former owner of a medical cab company in the Town of Wallkill in Orange County, NY, was sentenced Thursday to one to three years in prison for defrauding Medicaid of more than $200,000 by submitting falsified claims for medical transportation services, the Times Herald-Record reported.

Quitoni was arrested in September 2018. The New York State Attorney General’s Office, which prosecuted the case, argued that from 2013 to 2017, Quitoni submitted false claims seeking inflated payments from Medicaid. He was accused of submitting individual mileage claims for each Medicaid recipient traveling together in the same vehicle, instead of submitting group claims for mileage. Medicaid reimburses group trips at a lower rate per client than individual trips because the cost to providers is lower.

Quitoni was also accused of claiming Medicaid’s maximum allowance of $50 in toll reimbursement per trip, even though his vehicles did not incur that amount of toll expense. The Attorney General’s Office noted that there are no $50 tolls in New York and no combination of tolls on trips that Quatroni’s vehicles made which, when aggregated, could have totaled $50.

Continued Volatility Seen in Latest Edition of Value Index

Photo by Aaron Burden on Unsplash

Price volatility continued in the small-business transaction market during the second quarter of 2019, according to the latest edition of DealStats Value Index.

The median EBITDA multiple – the ratio of selling price to earnings before interest, taxes, depreciation and amortization – jumped to 4.2 for transactions completed in the second quarter, up from a median of 3.4 during the first three months of the year. That increase continued a trend of large quarterly swings that began during the second quarter of 2017.

DealStats is a database of private-company transactions maintained by Business Valuation Resources. The database is used by business appraisers when applying the market approach to valuation. Multiples such as sale price-to-EBITDA can be derived from transactions involving similar businesses and used to estimate the value of a company, subject to adjustments for unique characteristics of the company being valued.

Companies that sold during the second quarter were generally less profitable than those sold in the first quarter, according to Value Index. EBITDA represented 11 percent of revenue for second-quarter transactions, down from 15 percent for the first quarter of the year.

In short, transactions reported to DealStats for the second quarter featured companies that were less profitable (as measured by EBITDA) than those sold in the previous quarter, but they sold at higher multiples to the reduced earnings.

Not all sectors are created equal

What’s driving the increase in volatility? DealStats doesn’t offer any theories. One contributing factor could be a shift in the types of businesses sold from one quarter to the next. For instance, much has been written in recent years about consolidation in healthcare. Businesses in healthcare and social assistance sold at a median of 6.3 times EBITDA during the second quarter, among the highest multiples tracked by DealStats. Retailers, in contrast, sold for a median multiple of 3.8. A spate of medical practice mergers could drive up the overall multiple for a quarter. A run of retail acquisitions could drive it down.

The industries boasting the highest median EBITDA multiples during the second quarter were information at 11.1, and mining, quarrying and oil and gas extraction services at 8.3. The lowest EBITDA multiples were reported for transactions in accommodation and food services at 2.6, and other services at 3.0.

Size premium

The smallest of small businesses tend to enjoy the largest profit margins, but they garner the lowest multiples of that profit when they sell. The Value Index tracks this dynamic by dividing transactions into four groups based on net sales (less than $1 million, $1 million-$5 million, $5 million-$10 million and greater than $10 million).

Of those groups, businesses with less than $1 million in net sales have produced the highest net profit margins in each year since 2010, while businesses with sales of more than $10 million have generated the lowest margins in each year except 2011. This isn’t surprising, since the smallest businesses typically have limited overhead, and many are sole proprietorships with little payroll expense.

When small businesses are sold, however, the largest among them generate the highest price multiples. In 2018, the median ratio of selling price to EBITDA for businesses with sales greater than $10 million was a shade over 12, according to the Value Index. For those with sales of less than $1 million, the median was less than 4.

As we’ve noted before, larger businesses typically face less risk because they have more diversified products, vendors and customers. There’s an inverse relationship between risk and value. Larger businesses are rewarded with higher multiples in part because they are less risky.

Click below to read Advent’s recent article about size premiums in business valuation:

For pass-through entities, all items of income, loss, deduction and credit pass through to the owners’ individual tax returns, and taxes are paid at the personal level. Distributions to owners generally aren’t taxable to the extent that owners have positive tax basis in the entity.

For pass-through entities, all items of income, loss, deduction and credit pass through to the owners’ individual tax returns, and taxes are paid at the personal level. Distributions to owners generally aren’t taxable to the extent that owners have positive tax basis in the entity.