One way that business valuation

professionals can calculate the value of a business is by comparing it to

publicly traded companies whose value has been established by the market. But

how realistic is it to compare an independent five-store hardware chain – if

such a thing exists these days – to Home Depot and Lowe’s?

In an article first published in the August/September edition of Financial Valuation and Litigation Expert, William Quackenbush, director of Advent Valuation Advisors, explains the process of adjusting a guideline public company’s market multiples when valuing a closely held business. Click the link below to read “Quantitatively Adjusting Guideline Public Company Multiples.”

The father-and-son owners of an Orange County car dealership have been charged with tax fraud and bank fraud. Photo by Bill Oxford on Unsplash

The father-and-son operators of an Orange County used-car

dealership have been charged with understating their business’s income on tax

returns and overstating it on loan applications, according to the U.S. Attorney’s

Office for the Southern District of New York.

Mehdi Moslem and Saaed Moslem, owners of the Exclusive

Motor Sports car dealership in Central Valley, are accused of conspiring with a

tax preparer and others from 2009 to 2016 to conceal millions of dollars in

profits from the IRS.

Prosecutors say that in 2009, Saaed Moslem hired a tax

preparer in Rockland County who agreed to lower the yearend inventory value for

Exclusive, which increased Exclusive’s cost of goods sold and decreased the net

income reported on Saaed Moslem’s personal tax return. From 2010 to 2013 and again

in 2015, the defendants directed the tax preparer to use false information in

preparing partnership tax returns for Exclusive, according to the indictment.

The returns significantly understated gross receipts and underreported

inventory, thereby inflating the cost of goods sold. This reduced the business

income attributable to the men, resulting in the underpayment of personal

income taxes.

The tax preparer is not identified in the indictment, and

is referred to as CC-1, short for co-conspirator 1.

Prosecutors say Saaed Moslem used his fraudulent tax

returns to conceal his assets from creditors when he filed for bankruptcy in

2015. Both men are from Central Valley.

Bank

fraud

Prosecutors say that, from 2011 to 2017, the father

and son also conspired to defraud several financial institutions by submitting

inflated net worth statements and fabricated tax returns in support of loan applications.

They inflated the market value of their real estate holdings and omitted the

tax liabilities resulting from the understatement of their income on their

personal tax returns, according to the indictment. The loans included a $1.2

million mortgage on the car dealership property on which the men later

defaulted.

Mehdi Moslem, 70, and Saaed Moslem, 35, are each charged with one count of conspiracy to defraud the United States and one count of bank fraud conspiracy. Saaed Moslem is also charged with two counts of making false statements to a lender, and one count of concealing assets and making false declarations in a bankruptcy case.

When is no compensation considered reasonable compensation?

When an officer of a business is an officer in name only. That is one of the key takeaways of Davis v. United States, one of the landmark cases in the canon of compensation law.

This is the 25 anniversary of Davis v. United States, and Paul

Hamann and Jack Salewski recently penned a new analysis of the decision. While

the case is held out as the only reasonable compensation case the IRS has lost,

the authors argue that a nuanced analysis produces a more balanced view of the decision.

Then they offer some practical advice on putting the lessons

of Davis to work in assessing your firm’s – or your client’s – compensation.

Divorce cases involving family businesses can pose unique challenges. Photo by Kelly Sikkema on Unsplash

A

Connecticut appellate court recently delivered a resounding rebuke to a trial

judge for “double-dipping” in a divorce case.

The court hearing

the appeal in Oudheusden v. Oudheusden determined that the trial judge acted

unfairly in dividing the couple’s assets and setting alimony, despite warnings

from the lawyers for both sides regarding the risk of double-dipping.

According

to the appellate decision, Mr. Oudheusden built two businesses during the couple’s

decades-long marriage, and they represented his only sources of income. The

trial judge awarded Mrs. Oudheusden $452,000, representing half the fair market

value of the two businesses, as well as lifetime alimony of $18,000 per month.

In its decision, the appellate court stressed that the lump sum award and the stream of alimony payments were drawn from the same source.

“We agree

with the defendant that, under the circumstances of this case, the court

effectively deprived the defendant of his ability to pay the $18,000 monthly

alimony award to the plaintiff by also distributing to the plaintiff 50 percent

of the value of his businesses from which he derives his income,” the decision

reads. “The general principle is that a court may not take an income producing

asset into account in its property division and also award alimony based on

that same income.”

Second bite of the apple

In divorce

cases where the assets include a business, the value of the business and its

profitability are key considerations in dividing the estate. In Oudheusden v.

Oudheusden, the judge sided with the wife’s valuation expert in determining

that the businesses were worth a total of $904,000, and that the husband’s

annual gross income from them was $550,000.

Under the

income approach to valuing a closely held business, the valuation is derived by

calculating the present value of future benefits (often cash flow or some

variant thereof) that the business is expected to generate. First, the

business’s operating results are adjusted, or normalized, for nonrecurring or unrealistic

items. In many small, closely held businesses, it is not unusual for the amount

of compensation the business pays to its owner-operator to be motivated by tax

considerations. In such a case, a business appraiser should normalize the

owner’s compensation to reflect a fair market salary for the owner’s job

duties. This formalizes the distinction between the reasonable compensation for

the owner’s efforts and the business’s return on investment after deducting

that compensation.

Next, a

multiple of the normalized earnings is calculated based on the perceived risk

to the company’s future performance and the expected growth rate of its

earnings. The result of that calculation represents the present value of the

future benefits to be generated by the business.

When a

couple gets divorced, a judge who awards the nonowner spouse half the value of

the family business has in essence given that spouse half of the future

benefits to be generated by the business, discounted into today’s dollars.

Awarding alimony based on a percentage of the same future benefits to be

generated by the business would be taking a second bite from the apple, since

that stream of benefits has already been divided.

Mrs. Oudheusden’s

attorney explained the concept nicely in his closing statement, when he warned

the judge of the perils of double-counting a single stream of income:

“Whatever

value the court attributes to the business, the court has to, and should back

out a reasonable salary for the officer and owner of the company. Because if

the court is going to set a support order based on his income, it would not be

fair and equitable to also ask that he pay an equitable distribution based on

that as well,” he said. “That would be double-dipping.”

Decision reversed

After the trial court issued its decision, Mr. Oudheusden filed a post-judgment motion for clarification, asking if the judge considered $550,000 to be his income from his businesses, or his earning capacity if employed elsewhere. The judge responded that the figure was not a measurement of earning capacity, but rather of income from the two businesses.

The

appeals court found that the trial judge “failed to take into account that the

defendant’s annual gross income was included in the fair market value of his

businesses.”

The

appeals court also took issue with the trial court’s award of non-modifiable,

lifetime alimony, because it barred Mr. Oudheusden from seeking a modification

if he became ill or decided to retire, or if his businesses saw a reduction in their

earning capacity. But that is a topic for another day.

The

appeals court reversed the trial judge’s financial orders in their entirety and

returned the case for a new trial on those issues.

The

doctrine against double-dipping is largely settled law in many states,

including New York, where a substantial body of case law has refined its

application to various scenarios, such as the acquisition by one spouse of a

professional license during the marriage. Notable cases include McSparrow v.

McSparrow (Court of Appeals, 1995) and Grunfeld v. Grunfeld (Court of Appeals,

2000). That said, attorneys and valuation professionals who work in the

matrimonial arena should be aware of the potential for a poorly executed

valuation, or a misguided judge, to tilt the scales of justice.

Advent Valuation Advisors has a wealth of experience and a variety of research tools and resources at its disposal to help determine the value of a business and a reasonable salary for its owner-operator. For more information, contact Advent at info@adventvalue.com.

The owner of a French restaurant in Westchester County faces multiple fraud charges. Photo by Jez Timms on Unsplash

The owner of an upscale French restaurant in Westchester

County has been charged with multiple counts of fraud, accused of falsifying

bank records and running up an $80,000 tab on a customer’s credit card.

Barbara “Bobbie” Meyzen, owner of La Cremaillere

Restaurant in Banksville, faces a litany of fraud charges, the culmination of a

five-year spree of brazen acts of theft and fraud detailed by the U.S. Attorney’s

Office for the Southern District of New York.

Meyzen has owned the restaurant since 1993. From

August 2015 to July 2016, Meyzen submitted applications for credit on behalf of

the restaurant to at least nine lenders and factors. According to the U.S.

Attorney’s Office, Meyzen provided the potential lenders with business bank statements

that she had altered, changing negative balances to positive balances, removing

references to bounced checks and reducing service fees. When one lender discovered

that the bank statements had been altered, authorities say Meyzen created an

email account in the name of a bank officer and sent an email to the lender stating

that the bank statements were genuine.

Authorities say Meyzen falsely represented to the same

lender that the second mortgage on the restaurant had been paid off. She is accused

of forging a satisfaction of mortgage document, filing it with the Westchester

County Clerk’s Office and sending a copy to the lender. Meyzen later denied filing the false document,

telling FBI agents that she believed a loan broker with whom she had previously

worked had done it.

Meyzen is also accused

of charging more than $80,000 in food and restaurant supplies to the American

Express card of one of the restaurant’s customers. When the customer

discovered the charges, authorities say Meyzen claimed the charges were a

mistake and promised to resolve them. She later gave the customer two checks totaling

$32,000. The checks bounced. She told the FBI that she knew nothing about

the unauthorized charges and denied giving the customer any checks, according to

the U.S. Attorney’s Office.

In September 2018, Meyzen

Family Realty Associates, LLC, the company that owns the property where La Crémaillère operates, filed for bankruptcy in U.S.

Bankruptcy Court in White Plains. In April 2019, La Crémaillère Restaurant

Corp., which operates the restaurant, followed suit. Meyzen is a part owner in

both businesses. Two days after the second filing, Meyzen opened a bank account

in her name and diverted more than $40,000 of the restaurant’s credit card

receipts to that account, authorities said. The funds were used to make payments to a food distributor and to an in-home

nursing service.

That bank account was closed

on May 1. Six days later, Meyzen opened an account at another bank under Honey

Bee Farm, LLC, and diverted La Crémaillère’s credit card receipts, as well as

$20,000 in advances on the eatery’s future credit card revenue, to that account,

according to the U.S. Attorney’s Office. Authorities say Meyzen used some of

that money to make a payment on Meyzen Family Realty’s mortgage and to pay food

distributors, wine wholesalers, a commercial trash service, a tableware and

china company, and a restaurant employee.

Meyzen, 57,

of Redding, Connecticut, has been charged with aggravated identity theft, wire

fraud, mail fraud, credit card fraud, two counts of making false statements and

one count of concealing a debtor’s property.

Which of

these businesses do you think is riskier: A pizzeria on a busy street in some

village’s downtown business district, or a company with five pizzerias at

similar locations in five villages?

Chances are,

the single-location business faces more risk. Think of the effect a broken

water main would have on the day’s receipts, or the impact a new competitor

might have on foot traffic. Larger businesses tend to have more diversified

products, suppliers and customers, all of which mitigate risk.

Why is risk

important in business valuation? Because there is an inverse relationship

between risk and value. The greater the risk, the lower the value. That’s why

business valuation professionals often apply a size premium, also known as a

small-company risk premium, to capture the risks and the corresponding additional

returns investors expect to earn from the stock of small companies versus larger

ones.

How does this principle apply to small-business valuations?

In order to shed some light on this question, we analyzed data for small, private-company

transactions from 2003 to 2017 provided by Pratt’s Stats Private Deal Update for

the second quarter of 2018 (also known as Deal Stats Value Index). Valuation

professionals commonly employ these transactions to derive benchmark ratios, or

multiples, for use in the market approach to valuation.

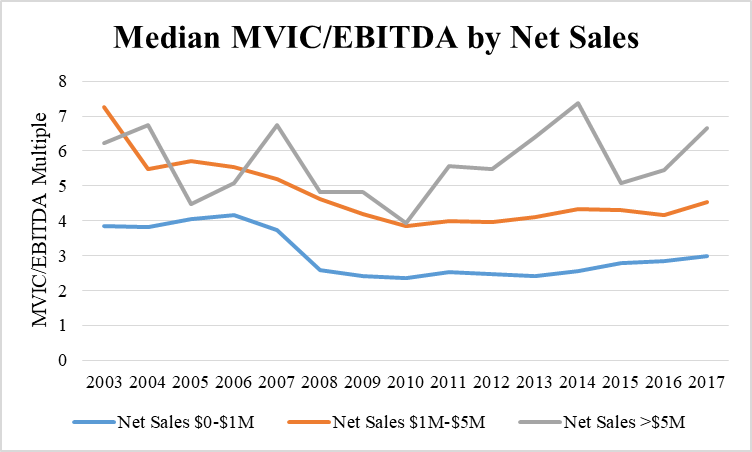

One such earnings multiple is MVIC/EBITDA. This is the ratio of the market value of invested capital (think “sale price”) to earnings before interest, taxes, depreciation and amortization, where invested capital equals equity plus debt. A business with $250,000 of EBITDA that sells for $1 million has an MVIC/EBITDA multiple of 4.

Private Deal Update provides median MVIC/EBITDA data by year

from 2003 to 2017 for companies in three net sales ranges: up to $1 million, $1

million to $5 million, and greater than $5 million.

The chart clearly shows that companies with the lowest net sales garnered significantly lower EBITDA multiples than did companies in the middle and upper sales ranges. Companies in the highest revenue range tended to sell at the highest multiples, with the distinction more pronounced since the end of the Great Recession. In 2017, the most recent year available, the largest companies sold at a median of 6.7 times EBITDA, compared to 4.5 times EBITDA for the middle range and 3 times EBITDA for the smallest companies.

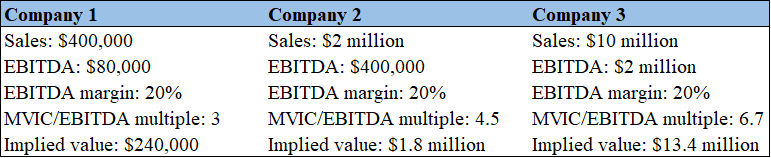

Consider a scenario in which those MVIC/EBITDA multiples are applied to three fictitious companies, each of which has a 20 percent EBITDA margin:

All three companies exhibit the same degree of profitability as measured

by EBITDA margin, but the small company’s implied value is just 60 percent of

annual sales, while the large company’s implied value is 134 percent of annual

sales.

The data provides a strong endorsement for the application of a size premium in transactions involving small businesses. As is often the case with sweeping pronouncements, however, there are caveats to bear in mind. We’ll leave you with a few:

The smallest companies in the dataset – those with up to $1 million in annual sales – tended to be more profitable than larger companies. This might mitigate, to some degree, the effect of their lower multiples.

There are many other factors beyond size – and beyond the scope of this article – that can affect a company’s valuation multiples.

And finally, the Private Deal Update data includes a melting pot of transactions in a variety of industries, from manufacturing to retail to IT. Each of these industries is made up of numerous subdivisions, each with unique characteristics, financial and otherwise.

Here at Advent, we won’t casually apply a broad analysis, but will drill down into the data to consider these unique characteristics and their impact on risk, and therefore value.

For more information, contact Advent Valuation Advisors at 845-567-0900

or info@adventvalue.com.

Ever wonder why a startup company that hasn’t turned a profit and may not even have a clear path to generating one can command a billion-dollar valuation?

What drives the value of these unicorns? Why are early investors so eager to pour money into them? Antonella Puca talks about the challenges of unicorn valuation and the importance of intangibles at aicpa.org.

The co-founder of a Manhattan investment firm and a former trader at the firm were convicted this week of inflating the value of the firm’s investments. Photo by Bill Oxford on Unsplash

The co-founder and CEO of a Manhattan investment firm

and a former trader at the firm were convicted Thursday of securities fraud.

Anilesh Ahuja, 51, the co-founder, CEO and chief investment officer of Premium Point Investments LP, which managed a portfolio of hedge funds, and Jeremy Shor, 44, a former trader at PPI, were convicted of scheming to artificially inflate the value of the firm’s holdings by more than $100 million in order to attract new investors and retain existing ones.

Ahuja, of New Rochelle,

NY, and Shor, of New York City, were found guilty of

all four counts against them: conspiracy

to commit securities fraud, which carries a maximum potential sentence of five

years in prison, and securities fraud, conspiracy to commit wire fraud, and

wire fraud, each carrying a maximum potential sentence of 20 years. The men will

be sentenced by U.S. District Judge Katherine Polk Failla at a future date.

Before founding PPI a decade ago, Ahuja was the head

of the residential mortgage-backed securities group at a global investment

bank. At its peak, PPI managed more than $5 billion in assets.

According to prosecutors, from approximately 2014 to

2016, Ahuja and Shor participated in a conspiracy to defraud PPI’s investors and

potential investors by mismarking the value of certain securities held by its

funds each month, thereby inflating the net asset value of those funds as

reported to existing and potential investors.

Two former PPI employees, Amin Majidi of Armonk and

Ashish Dole of White Plains, had already pleaded guilty to their roles in the

scheme, as had Frank Dinucci Jr., a former salesman at a broker-dealer.

“Investors in our markets must be able to count on the truth and accuracy of the information they receive from those they entrust with their money,” said Deputy U.S. Attorney Audrey Strauss.

To read the U.S. Attorney’s Office’s press release on the conviction: justice.gov/usao-sdny

To read the U.S. Attorney’s Office’s press release on the indictment of Ahuja, Majidi and Shor: justice.gov/majidi

New standards released Wednesday by the American Institute of Certified Public Accountants provide guidance for member engagements involving investigation or litigation.

The American Institute of Certified Public Accountants on Wednesday issued its first authoritative standards for members who provide forensic accounting services.

Forensic accounting services are described in the document as those involving “the application of specialized knowledge and investigative skills by a member to collect, analyze, and evaluate certain evidential matter and to interpret and communicate findings.” The Statement on Standards for Forensic Services No. 1 focuses on certain types of engagements – litigation and investigation – rather than the specific skill sets used or activities involved in those engagements.

Litigation is described in the statement as “an actual or potential legal or regulatory proceeding before a trier of fact or a regulatory body as an expert witness, consultant, neutral, mediator, or arbitrator in connection with the resolution of disputes between parties.” The category includes disputes and alternative dispute resolution.

Investigation is described as “a matter conducted in response to specific concerns of wrongdoing in which the member is engaged to perform procedures to collect, analyze, evaluate, or interpret certain evidential matter to assist the stakeholders in reaching a conclusion on the merits of the concerns.”

The standards generally do not apply to forensic services performed as part of an attest engagement such as an audit, review or compilation, or to internal assignments made by an employer to an employee not in public practice.

Under the standards, an AICPA member who serves as an expert witness in a litigation engagement is generally barred from providing opinions subject to contingent fee arrangements. A member performing forensic services is also prohibited from issuing an opinion regarding whether a fraud has been committed. A member may provide an expert opinion regarding “whether evidence is consistent with certain elements of fraud or other laws.”

The standards were developed and issued by the AICPA’s Forensic and Valuation Services Executive Committee. They are effective for engagements accepted on or after January 1, 2020, but may be voluntarily implemented earlier. Member forensic services are also subject to the AICPA’s broader “General Standards Rule,” which establishes guidelines such as professional competence, professional care and planning and supervision.

If you have any questions regarding this article or other matters related to forensic accounting, please contact Advent Valuation Advisors at info@adventvalue.com.

Business Brokers Note Dip in Seller Confidence in First Quarter

Seller sentiment declined during the first quarter in four out of five price segments below $50 million, according to a survey of business brokers and M&A advisors. Photo by rawpixel.com from Pexels

It’s still a seller’s market, but the balance of power in business transactions has begun to shift, according to the latest edition of Market Pulse, the quarterly survey of business brokers conducted by the International Business Brokers Association and M&A Source.

The national survey is intended to capture market conditions for businesses being sold for less than $50 million. It divides that market between Main Street businesses with values of $2 million or less, and lower middle-market ones in the $2 million to $50 million range.

The report for the first quarter of 2019 describes a robust market in which sellers of businesses hold the advantage in all segments except the smallest (under $500,000). But it also notes that seller confidence declined over the preceding year across all market segments except for the $5 million to $50 million value range.

A seller’s market is reflected in seller confidence in excess of 50 percent.“Although it is still a strong seller’s market with strong values, this is the first time in years that we’ve seen four out of five sectors report a dip in seller market sentiment,” said Craig Everett, PhD, who is quoted in the report. Everett is director of the Pepperdine Graziadio Business School’s Private Capital Markets Project, which compiled the survey’s results. “This is a sign the market has peaked, and more people are expecting a correction in the year or two ahead.”

The first-quarter survey of 292 business brokers and M&A advisors was conducted from April 1-15.

Other takeaways from the report include:

Larger companies are selling at higher multiples than smaller ones. During the first quarter, sales for less than $500,000 carried a median multiple of price to seller’s discretionary earnings of 2.0. Businesses in the $1 million to $2 million range sold for three times SDE. The median EBITDA multiple paid for businesses in the $2 million to $5 million range was 4.3, compared to the median multiple of 6.0 for businesses in the $5 million to $50 million range.

Larger companies tend to sell for a greater percentage of asking price. Lower middle-market companies ($5 million to $50 million in value) sold for 101 percent of the asking price or internal benchmark. Small Main Street companies (less than $500,000) sold for 85 percent of asking price.

One reason for the difference: Larger companies are more likely to attract interest from private equity or synergistic buyers, according to David Ryan of Upton Financial Group, who is cited in the report.

Smaller businesses also tend to depend more heavily on their owners, which means more value is lost when the owner leaves the business. For more information on the report, go to: https://www.ibba.org/market-pulse