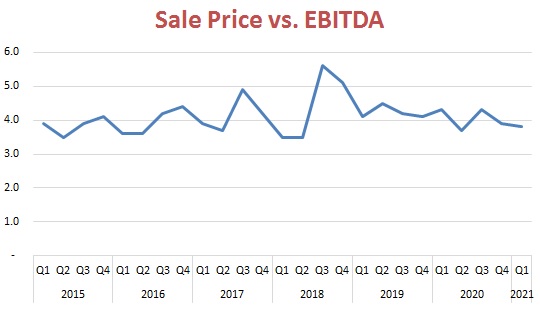

The median price-to-EBITDA multiple among deals reported to DealStats fell slightly to 3.8 during the first quarter of 2021, down from 3.9 in the fourth quarter of 2020, suggesting transaction prices remain under pressure from the coronavirus pandemic.

According to the latest edition of DealStats Value Index, the four-quarter average EBITDA (earnings before interest, taxes, depreciation and amortization) multiple for the year ending in March 2021 was 3.9, the lowest such average since the period ending in the third quarter of 2016.

EBITDA measured as a percentage of net sales fell to 10 percent in the first quarter of 2020, due at least in part the ongoing economic toll of the pandemic and resulting restrictions. The reduction also reflects a longer-term trend of lower margins. EBITDA margins for transacted businesses have fluctuated between roughly 10.5 percent and 12 percent since late 2018, according to DealStats. From 2015 to 2018, they generally moved between 11 percent and 14.5 percent. DealStats does not indicate if the EBITDA margin metric is a median or an average.

Transaction reporting appears to have slowed with the pandemic. Of 15 sectors tracked by DealStats, just three met the minimum of 10 reported transactions during the first quarter required for the inclusion of sector-specific multiples.

DealStats is a database of private-company transactions maintained by Business Valuation Resources. The database is used by business appraisers when applying the market approach to valuation. Multiples such as sale price-to-EBITDA can be derived from transactions involving similar businesses and used to estimate the value of a company, subject to adjustments for unique characteristics of the business being valued.

There are many factors to consider when determining reasonable owners’ compensation. Photo by Matthew Henry from Burst

For most privately held businesses, owners’ compensation is one of the largest expenses on the income statement, especially when all the related perks and hidden costs are calculated. Compensation should accurately reflect what others would receive for similar duties in a similar setting. Reasonable compensation levels are important not only for state and federal tax purposes, but also to get an accurate estimate of the fair market value of the business.

Total Compensation Package

Before compensation can be assessed as reasonable, all components of the package must be calculated, including:

Direct salaries, bonuses and commissions,

Stock options and contingent payments,

Payouts under golden parachute clauses,

Shareholder loans with low (or no) interest and other favorable terms,

Company-owned or leased vehicles and vehicle allowances,

Moving and relocation expenses,

Subsidized housing and educational reimbursements,

Excessive life insurance or disability payments, and

Other perks, such as cafeteria plans, athletic club dues, vacations and discounted services or products.

In addition, owners’ compensation may be buried in such accounts as management and consulting fees, rent expense and noncompete covenants.

IRS Guidance

The IRS has published a guide titled, “Reasonable Compensation: Job Aid for IRS Professionals.” IRS field agents use this guide when conducting audits to help determine what’s reasonable and how to estimate an owner’s total compensation package.

The IRS is on the lookout for C corporations that pay employee-shareholders excessive salaries in place of dividends. This tactic lowers the overall taxes paid, because salaries are a tax-deductible expense and dividends aren’t.

Owner-employees of C corporations pay income tax on salaries at the personal level, but dividends are subject to double taxation (at the corporate level and at each owner’s personal tax rate). If the IRS decides that a C corporation is overpaying owners, it may reclassify part of their salaries as dividends.

For S corporations, partnerships and other pass-through entities, the IRS looks for businesses that underpay owners’ salaries to minimize state and federal payroll taxes. Rather than pay salaries, S corps are more likely to pay distributions to owners. That’s because distributions are generally tax-fee to the extent that the owner has a positive tax basis in the company.

The IRS job aid lists several sources of objective data that can be used to support compensation levels, including:

General industry surveys by Standard Industry Code (SIC) or North American Industry Classification Systems (NAICS),

Salary surveys published by trade groups or industry analysts,

Proxy statements and annual reports of public companies, and

Private company compensation reports such as data published by Willis Towers Watson, Dun & Bradstreet, the Risk Management Association or the Economic Research Institute.

“Reasonable and true compensation is only such amount as would ordinarily be paid for like services by like enterprises under like circumstances,” states the IRS job aid.

Compensation Benchmarks

Beyond IRS audits, the issue of reasonable compensation may become an issue in shareholder disputes, marital dissolutions and other litigation matters. When valuing a business for these purposes, a company’s income statement may need to be adjusted for owners’ compensation that is above or below market rates.

Courts often rely on market data to support owners’ compensation assessments. But it can be a challenge to find comparable companies — and comparable employees within those companies. The five areas that courts consider when evaluating reasonable compensation are:

The individual’s role in the company,

External comparisons of the salary with amounts paid to similar individuals in similar roles,

Character and condition of the company,

Potential conflicts of interest between the individual and the company, and

Internal inconsistency in the way employees are treated within the organization.

Owners can control compensation, and that creates an inherent conflict of interest when estimating what’s reasonable. External comparisons are key to supporting compensation levels. Business valuation experts typically interview owners to get a clearer picture of their experience, duties, knowledge and responsibilities.

Get It Right

For more information about reasonable owners’ compensation, please contact the business valuation professionals at Advent Valuation Advisors. We can help estimate total compensation levels, find objective market data and adjust deductions that are above or below market rates.

Make your business sparkle – and tidy up the books, too – to help ensure a successful sale. Photo by Verne Ho on Unsplash

The COVID-19 pandemic has put unprecedented stress on private business owners. Some are now considering selling their businesses before Congress has a chance to increase the rates on long-term capital gains. Before putting your business on the market, it’s important to prepare it for sale. Here are six steps to consider.

1. Clean Up the Financials

Buyers are most interested in an acquisition target’s core competencies, and they usually prefer a clean, simple transaction. Consider buying out minority investors who could object to a deal and removing nonessential items from your balance sheet. Items that could complicate a sale include underperforming segments,nonoperating assets, andshareholder loans.

Sales are often based on multiples of earnings or earnings before interest, taxes, depreciation and amortization (EBITDA). Do what you can to maximize your bottom line. That includes cutting extraneous expenses and operating as lean as possible.

Buyers also want an income statement that requires minimal adjustments. For example, they tend to be leery of businesses that count as expenses personal items (such as country club dues or vacations) or engage in above-or below-market related party transactions (such as leases with family members and relatives on the payroll).

2. Highlight Strengths and Opportunities

Private business owners nearing retirement may lose the drive to grow the business and, instead, operate the company like a “cash cow.” But buyers are interested in a company’s potential. Achieving top dollar requires a tack-sharp sales team, a pipeline of research and development projects and well-maintained equipment. It’s also helpful to have a marketing department that’s strategically positioning the company to take advantage of market changes and opportunities, particularly in today’s volatile market conditions.

3. Downplay (or Eliminate) Risks

It’s no surprise that businesses with higher risks tend to sell for lower prices. No company is perfect, but industry leaders identify internal weaknesses (such as gaps in managerial expertise and internal control deficiencies) and external threats (such as increased government regulation and pending lawsuits). Honestly disclose shortcomings to potential buyers and then discuss steps you have taken to mitigate risks. Proactive businesses are worth more than reactive ones.

4. Prepare a Comprehensive Offer Package

Potential buyers will want more than just financial statements and tax returns to conduct their due diligence. Depending on the industry and level of sophistication, they may ask for such items as:

Marketing collateral,

Business plans and financial projections,

Fixed asset registers and inventory listings,

Lease documents,

Insurance policies,

Franchise contracts,

Employee noncompete agreements, and

Loan documents.

Before you give out any information or allow potential buyers to tour your facilities, enter into a confidentiality agreement to protect your proprietary information from being leaked to a competitor.

5. Review Deal Terms

Evaluate different ways to structure your sale to minimize taxes and maximize selling price. For example, one popular element is an earnout, where part of the selling price is contingent on the business achieving agreed-upon financial benchmarks over a specified time. Earnouts allow buyers to mitigate performance risks and give sellers an incentive to provide post-sale assistance.

Some buyers also may ask owners to stay on the payroll for a period of time to help smooth the transition. Seller financing and installment sales also are commonly used.

6. Hire a Valuator

A fundamental question buyers and sellers both ask is what the company is worth in the current market. To find the answer, business valuation professionals look beyond net book value and industry rules of thumb.

For instance, a business valuation professional can access private transaction databases that provide details on thousands of comparable business sales. These “comparables” can be filtered and analyzed to develop pricing multiples to value your business.

Alternatively, a valuation expert might project the company’s future earnings and then calculate their net present value using discounted cash flow analyses. These calculations help buyers set asking prices that are based on real market data, rather than gut instinct. However, final sale prices are influenced by many factors and can be higher or lower than a company’s appraised value.

They can also estimate the value of buyer-specific synergies that result from cost-saving or revenue-boosting opportunities created by a deal. Synergistic expectations entice buyers to pay a premium above fair market value.

Planning for a Sale

Operating in a sale-ready condition is prudent, even if you’re not planning on selling your business anytime soon. Our experiences in 2020 have taught us to expect the unexpected: You never know when you’ll receive a purchase offer, and some transfers are involuntary.

The professionals at Advent can help you prepare for a sale whether in 2021 or beyond.

While not a New York case, a recent divorce case in Delaware Family Court sheds new light on an old precedent for the treatment of enterprise goodwill in a sole proprietorship.

The couple in A.A. v. B.A. married in 1979 and divorced in February 2017, but the case lingered, with a decision regarding the valuation of the husband’s financial advisory practice, a sole proprietorship, coming in October 2020.

Both spouses hired experts to value the business. The experts reached widely divergent conclusions, with the husband’s expert valuing the business at $255,000, while the wife’s arrived at a value of $3,488,0000 to $3,500,000.

The court rejected the report by the husband’s expert, taking issue with both its failure to consider the business’s goodwill and its reliance on a flawed asset approach.

“From the outset, husband’s expert’s opinion was limited by his belief that Delaware law was settled that there could not be good will in a sole proprietorship,” reads the decision.

The husband’s expert had relied on a 1983 Delaware Supreme Court decision. In E.E.C. v. E.J.C., (457 A. 2d 688, Del. 1982), the court had rejected the consideration of goodwill in the valuation of a sole practitioner’s law practice. According to the decision in A.A. v. B.A., the husband’s expert took that oft-cited decision as an indication that Delaware case law does not permit the use of goodwill in valuing sole proprietorships under any circumstances.

The court rejected this premise: “The court notes that husband’s business in the present case is not a law firm and the practice and means of generating income are different. The court does not read E.E.C. as stating every sole proprietorship in every case has no professional good will.”

The court agreed with the wife’s expert, who assigned 5 percent of the total goodwill to the husband based on the value of his noncompete agreement, and the remaining 95 percent to the business. The court said both experts agreed that, if the husband could transfer goodwill such that he could transfer to a buyer his client base and stream of income, or even 95 percent of his stream of income, he could receive about $3.5 million for the business.

Misassessed assets

The court also took issue with the husband’s expert’s asset approach, which did not consider income earned but not yet paid to the business as of the separation: “Husband continued to run the business and the value receive[d] by husband through receivables, work in process or residual commission tails was well beyond the amount placed on it by husband’s expert. This would probably explain why the husband himself placed a value of $10 million on the business in his financial statements.”

The decision notes that, between the date of separation and late 2019, the husband extracted more than $4 million from the business, including commissions for work done during the marriage. This included a $600,000 commission received in 2018 that had been in the making for perhaps three years, according to the husband’s testimony.

The wife’s expert used a weighted combination of the income approach (capitalized income method) and market approach (transaction and guideline public company methods). The court relied on the wife’s expert, determining that the business’s value was $3,488,000.

The case is A.A. v. B.A., CN16-05018 (Del. Fam. Oct. 9, 2020). Read the decision here.

* * *

If you require assistance with the valuation of your business in a matrimonial matter, please contact Advent for trusted guidance.

A smartly crafted buy-sell agreement can spare you and your business from complications down the road. Photo by Marcelo Dias from Pexels

When a business is owned by more than one person, it’s generally advisable for the owners to enter into a contractual agreement that prescribes what will happen if an owner dies, becomes disabled, retires or otherwise leaves the company.

Some market analysts predict that the COVID-19 crisis may trigger an increase in buyouts. For example, some struggling owners may decide to throw in the towel after months of teetering on the verge of bankruptcy. Or squabbling partners may disagree about the future of the business and decide to part ways.

So, now is a good time for owners to draft or update a buy-sell agreement. Here’s a look at common valuation issues and potential pitfalls to avoid.

Valuation Considerations

“Buy-sells,” as they’re often called, may be standalone agreements or a provision within a broader agreement (such as a partners’ or shareholders’ agreement). To avoid misunderstandings and delays when redeeming a departing owner’s interest, a buy-sell should address the following key elements:

Appropriate standard of value (such as fair market value or fair value)

Definition of the standard of value

List of applicable valuation adjustments and discounts

Relevant method of quantifying valuation adjustments and discounts

Effective date of the valuation (for example, the year-end nearest the triggering event)

Buyout terms (including who will buy the interest and how payments will be made), and

Appraisal/redemption deadline (for example, within 30 or 90 days of the triggering event).

The buy-sell should also specify the parties’ preferred method of appraisal. Examples include a fixed price, a prescribed formula or the use of credentialed business valuation professionals.

In some cases, the owners agree to use the company’s CPA firm to perform an independent valuation of the departing owner’s interest. Other buy-sells require two outside appraisals: one for the buyer and another for the seller; the value of the departing owner’s interest is then determined by averaging the results of the two conclusions.

Potential Pitfalls

Ambiguous or outdated buy-sells can cause problems when it’s time for a buyout. For example, an agreement containing undefined valuation terminology — such as “earnings” or “value” — may be subject to different interpretations.

Likewise, the use of a prescribed formula that’s based on a simplistic industry rule of thumb might cause problems when a buyout happens several years after the agreement was executed. Industry and economic conditions may have changed, or the company’s product or service lines might have evolved.

For instance, some companies have pivoted during the COVID-19 crisis to take advantage of new market opportunities, automate certain processes, or minimize face-to-face interactions with customers.

Fixed valuation formulas that were valid before the pandemic may no longer be relevant in the new normal. This underscores the importance of creating a “living” buy-sell that’s reviewed and updated regularly to stay current.

One More Word of Caution

During a buyout, the buyer is typically either the company or the remaining owners. The seller is usually either the departing owner or the departing owner’s heirs. Because the buyer controls how financial results are reported after the seller leaves the business, the seller should be wary of the potential for financial misstatement. Financial statements often are used to value the departing owner’s interest. So, the buyer has an incentive to understate revenue and assets or overstate expenses and liabilities. These manipulations can lower the buyout price, unless adjustments are made to the company’s financial statements.

Outside Expertise

There is no one-size-fits-all buy-sell agreement. The input of a business valuation professional when drafting or updating a buy-sell can help achieve the owners’ buyout objectives and reduce disputes when and if the agreement is triggered. If you have any questions, the professionals at Advent Valuation Advisors are here to help.

For more information on buy-sell agreements, read our previous blog post here.

Determining the effects of the COVID-19 pandemic on the value of a business may involve a high degree of complexity. Photo by Sarah Pflug from Burst

Business valuation is a prophecy of the future. That is, investors typically value a business based on its ability to generate future cash flow. However, with so many uncertainties in the current marketplace, forecasting expected cash flow can be challenging.

Income Approach

Under the income approach, the value of a business interest is a function of two variables:

1. Expected economic benefits, and

2. A discount rate based on the risk of the business.

Economic benefits can take many forms, such as earnings before tax, cash flow available to equity investors and cash flow available to equity and debt investors. Likewise, discount rates can take many forms. Examples include the cost of equity or the weighted average cost of capital (WACC).

Common valuation methods falling under the income approach include:

Capitalization of earnings. Under this method, economic benefits for a representative single period are converted to present value through division by a capitalization rate. The cap rate equals the discount rate minus a long-term sustainable growth rate. This technique — sometimes referred to as the capitalized cash flow (CCF) method — is generally most appropriate for mature businesses with predictable earnings and consistent capital structures. It’s also commonly used to value real estate with a predictable stream of net operating income.

Discounted cash flow (DCF). This method derives value by discounting a series of expected cash flows. The “cash flow” at the end of the forecast period is known as the terminal (or residual) value. Terminal value is typically calculated using the market approach or the capitalization of earnings method. It represents how much the company could be sold for at the end of the forecast period, when the company’s operations have, in theory, stabilized.

DCF models are generally more flexible than the capitalization of earnings method. For example, the DCF method is well-suited for high-growth companies and those that expect to alter their capital structure over the short run.

Adjusting for COVID-19 Impact

During the pandemic, many valuation professionals are using DCF models, rather than the capitalization of earnings method, to better capture temporary changes in the marketplace. In addition to detrimental effects of the pandemic, these temporary changes may include benefits from government loans or grants. The appropriate time frame for a DCF analysis depends on how long the subject company expects its operations to be disrupted. Some experts are using two- or three-year DCF models; others prefer to use a longer time frame.

In addition, it’s important for valuators not to double-count COVID-19-related risk factors in both the company’s expected economic benefits and the discount rate.

Evaluating Inputs

A business valuation is only as reliable as the inputs on which it’s based. Business valuation professionals typically rely on management to prepare forecasts. But, in the COVID-19 era, those estimates may not necessarily be reliable. That’s because managers tend to use the prior year’s results as the starting point for forecasting the current year. Then it’s assumed that revenue, variable expenses and working capital will grow at a moderate rate, while fixed expenses will largely remain constant.

However, these simplistic models may no longer be valid in today’s volatile, evolving marketplace. Many businesses — including resorts and casinos, sports venues, schools and movie theaters — have temporarily shut down or scaled back operations during the pandemic. Others are using new methods of distribution or devising pivot strategies to stay afloat. Examples include doctors and therapists who are providing telehealth services, restaurants and retailers that are offering online ordering, delivery and curbside pick-up, and food-processing facilities that are selling directly to consumers rather than to cruise lines and high-end restaurants.

In addition, cost structures have changed for many types of businesses. For example, most white-collar workers are working from home instead of commuting to offices, people of all ages are converting from in-person to online learning, companies are eliminating nonessential travel, and some organizations have become increasingly reluctant to work with overseas suppliers. In the face of a contentious, divisive presidential election, there is also significant uncertainty about the future of federal tax laws and other government regulations.

Which changes will be temporary, and which will last beyond the COVID-19 crisis? No one has a crystal ball, but it’s likely that some changes — including work-from-home arrangements and other cost-cutting measures — will be part of the new normal. Other aspects of everyday life — such as attending sporting events, going on vacations and dining out — are expected to eventually return to normal. But it’s still unclear how long recovery will take.

So, before discounting expected earnings, it’s important to evaluate whether management’s forecasts seem reasonable. Oversimplified models and unrealistic assumptions can lead to valuation errors.

Outside Expertise

Estimating how much cash flow a business will generate is no easy task in today’s unprecedented conditions. A trained valuation professional is atop the latest trends and economic predictions and can help management create comprehensive forecasts that are supported by market evidence, rather than gut instinct and oversimplified assumptions.

The professionals at Advent Valuation Advisors stand ready to help you understand the implications of the pandemic on the value of your business. For more information, please contact us.

More than 140 lawsuits have been filed against insurers over claims for business interruptions caused by the COVID-19 pandemic. Photo by Matthew Henry from Burst

An insurer scored a significant win in what is believed to be the first court decision involving a COVID-19-related business interruption claim.

On July 1, 2020, 30th Circuit Judge Joyce Draganchuk in Ingham County, Michigan, dismissed a lawsuit by the owner of two restaurants in Lansing Michigan, siding with the insurer’s decision to deny a claim for business-interruption coverage because the eateries did not sustain “direct physical loss or damage.”

The decision in Gavrilides Management Company v. Michigan Insurance Co. was previously reported by the National Law Review, among others. Gavrilides Management sought $650,000 from Michigan Insurance Co. for losses it sustained after Gov. Gretchen Whitmer issued executive orders in March that limited its two restaurants to delivery and take-out orders.

Judge Draganchuck said it is clear from the wording of the insurance policy that only direct physical loss to the properties is covered. She rejected as “simply nonsense” the plaintiff’s claim that the restaurants were damaged “because people were physically restricted from dine-in services.”

“Direct physical loss of or damage to the property has to be something with material existence, something that is tangible, something … that alters the physical integrity of the property. The complaint here does not allege any physical loss of or damage to the property,” the judge said during the July 1 video court session. “The complaint alleges a loss of business due to executive orders shutting down the restaurants for dining … in the restaurant due to the COVID-19 threat, but the complaint also states that, at no time has COVID-19 entered the Soup Spoon or the Bistro through any employee or customer.”

The judge noted that the insurance policy also has a virus and bacteria exclusion, and that loss of access to the premises due to government action is not covered.

You can watch a recording of the virtual court appearance here.

Testing the Limits of Coverage

Business interruption insurance typically covers the loss of income that a business suffers due to the disaster-related closing of the business and the rebuilding process after a disaster. The COVID-19 pandemic is testing the limits of this coverage and its applicability to unprecedented circumstances. Countless businesses were forced to close as a result of the COVID-19 pandemic and the ensuing emergency orders. While many businesses have been able to reopen since, often on a limited basis, the losses sustained have been steep and, in many cases, ongoing.

Several state legislatures, including New York’s, have introduced bills that would require insurers to cover business-interruption losses stemming from COVID-19, even if the policies specifically exclude such coverage. Meanwhile, more than 140 COVID-19-related business interruption cases have been filed in federal courts nationwide, including several filed in U.S. District Court for the Southern District of New York. To read three of the complaints, click on the links below.

Advent Valuation Advisors provides a variety of litigation support services, including the assessment of damages from business interruption. For more information on business interruption claims, read our blog posts here and here. If you have any questions, please contact us.

Business valuations completed in connection with divorce proceedings can be especially complex. Photo by Kelly Sikkema on Unsplash

The South Carolina State Supreme Court weighed in recently on the long-simmering tension between recognized standards of business valuation and the goal of equity in dividing marital assets in divorce proceedings.

The decision In Clark v Clark (Appellate Case No. 2019-000442), addresses the division of marital assets, specifically the valuation of a minority interest in a family business. The Supreme Court reiterated a lower court’s assertion that the applicability of discounts for lack of control (DLOC) and marketability (DLOM) are to be determined on a case-by-case basis, then affirmed one part of that court’s ruling regarding discounts and reversed another.

The Family Business

George and Patricia Clark were married in 1987. During the marriage, Mr. Clark began working for the family business, Pure Country, a manufacturer of custom tapestry blankets and other items. His father founded the business and eventually transferred his 75 percent interest in it to Mr. Clark. A family court determined at the time that the transfer was a gift, and therefore the interest was not marital property. Mr. Clark purchased the remaining 25 percent of the business from his sister. In 2009, he transferred a 25 percent interest to Mrs. Clark. The related stock agreement limited any subsequent sale of that interest to other shareholders, immediate family members or the business.

In 2012, Mr. Clark filed for divorce. Both spouses hired experts to value Mrs. Clark’s interest in the business. The husband’s expert applied a DLOC and a DLOM. In support of the DLOM, she noted that the sale of interests in privately held companies require more time and resources and involve higher transaction costs than do sales of publicly traded interests. She also considered the restrictive language in the stock agreement from the 2009 transfer.

The wife’s expert applied a smaller DLOM, but later argued that the value should not be discounted at all. He did not apply a DLOC.

The family court found the husband’s expert more credible and agreed with her use of discounts. While it did acknowledge the “debate as to whether … discounts should apply in a divorce setting as the business is actually not being sold,” the court recognized that the valuation standard in such cases is fair market value, which assumes a hypothetical transaction between two willing parties.

Mrs. Clark appealed the decision to the court of appeals, which agreed that a minority shareholder would not have control over the company and therefore upheld the family court’s decision to apply a DLOC, but reduced the size of the discount. The court of appeals rejected the DLOM, noting the husband did not intend to sell the business and relying on a precedent set in Moore v Moore. “To the extent the marketability discount reflected an anticipated sale, Moore deems it a fiction South Carolina law no longer recognizes.” The court found that because the husband did not plan to sell the business, the restriction on transfers of stock was moot.

The decision compelled both parties to file appeals to the State Supreme Court.

Split Decision

The husband argued that the court of appeals erred in rejecting the DLOM when each party’s expert had applied one. The wife contended that the DLOM should not be considered because a DLOM accounts for the higher transaction costs inherent in the sale of an interest in a private company, and her husband did not intend to sell.

The Supreme Court affirmed the family court’s decision to apply a DLOM and a DLOC and the appeals court’s decision to reduce the DLOC. The decision states that a party’s interest in a closely held company is valued based on its fair market value, which has been well established as “the amount of money which a purchaser willing but not obligated to buy the property would pay an owner willing but not obligated to sell it, taking into account all uses to which the property is adapted and might in reason be applied.”

That said, the court acknowledges the tension between this principle of valuation and “the desire to fairly and justly apportion marital assets.” The court refuses to draw a bright line on the issue, stating that the applicability of such discounts is to be determined on a case-by-case basis. The Supreme Court’s decision was not unanimous. Two of the five justices issued a dissenting opinion rejecting the application of either discount, stating that “under certain facts, faithful adherence to the concept of fair market value must yield to reality.”

The decision, while not directly applicable to New York cases, speaks to the complexities involved in divorce-related valuations and the need for valuation professionals to weigh competing considerations. If you have questions regarding the valuation issues in a divorce or another context, Advent’s professionals are here to help.

Recent changes to U.S. Bankruptcy Law may provide additional relief for some struggling businesses. Photo by Melinda Gimpel on Unsplash

The novel coronavirus pandemic has caused many businesses to temporarily shut down or scale back operations. Slowly, states are allowing businesses to reopen to the public. But it may be too late for some businesses to bounce back. As a result, the number of businesses filing for bankruptcy is expected to skyrocket this summer.

Two recent changes to the U.S. Bankruptcy Code may provide greater relief for small businesses that seek to use the bankruptcy process to reorganize their finances and continue operating. The Small Business Reorganization Act (SMRA) increases access to Chapter 11 for small businesses. The Coronavirus Aid, Relief, and Economic Security (CARES) Act raises the debt threshold that qualifies for this protection. Here’s what small business owners should know.

SMRA Basics

Effective on February 19, 2020, the SMRA creates a new subchapter (Subchapter V) of the Bankruptcy Code. To be eligible for relief under Subchapter V, a debtor, whether an entity or an individual, must have total debt not exceeding $2,725,625 (subject to adjustment every three years). The SMRA contains provisions for the following key improvements:

Streamlined reorganizations: The new law will facilitate small business reorganizations by eliminating certain procedural requirements and reducing costs. Significantly, no one except the business debtor will be able to propose a plan of reorganization. Plus, the debtor won’t be required to obtain approval or solicit votes for plan confirmation. Absent a court order, there will be no unsecured creditor committees under the new law. The new law also will require the court to hold a status conference within 60 days of the petition filing, giving the debtor 90 days to file its plan.

New value rule: The law will repeal the requirement that equity holders of the small business debtor must provide “new value” to retain their equity interest without fully paying off creditors. Instead, the plan must be nondiscriminatory and “fair and equitable.” In addition, similar to Chapter 13, the debtor’s entire projected disposable income must be applied to payments or the value of property to be distributed can’t amount to less than the debtor’s projected disposable income.

Trustee appointments: A standing trustee will be appointed to serve as the trustee for the bankruptcy estate. The revised version of Chapter 11 allows the trustee to preside over the reorganization and monitor its progress.

Administrative expense claims: Currently, a debtor must pay, on the effective date of the plan, any administrative expense claims, including claims incurred by the debtor for goods and services after a petition has been filed. Under the new law, a small business debtor is permitted to stretch payment of administrative expense claims over the term of the plan, giving this class of debtors a distinct advantage.

Residential mortgages: The new law eliminates the prohibition against a small business debtor modifying his or her residential mortgages. The debtor has more leeway if the underlying loan wasn’t used to acquire the residence and was used primarily for the debtor’s small business. Otherwise, secured lenders will continue to have the same protections as in other Chapter 11 cases.

Discharges: The new law provides that the court must grant the debtor a discharge after completing payments within the first three years of the plan or a longer period of up to five years established by the judge. The discharge relieves the debtor of personal liability for all debts under the plan except for amounts due after the last payment date and certain nondischargeable debts.

CARES Act Provision

In addition to the improvements under the SMRA, Congress decided to temporarily increase the debt ceiling for eligibility to $7,500,000 from $2,725,625 for new Subchapter V cases filed between March 28, 2020, and March 27, 2021. Thereafter, the debt limit will revert to $2,725,625.This change will make more small businesses eligible for Chapter 11 in the midst of the novel coronavirus crisis. However, the CARES Act permanently eliminates the eligibility to file for Subchapter V relief for any affiliate of a public company.

We Can Help

Businesses contemplating bankruptcy often benefit from the input of an experienced business valuation expert. Specialists with experience in accounting, valuation and mergers and acquisitions can help assess the severity of the financial crisis, determine whether liquidation or reorganization makes sense, and provide financial insight on everything from selling assets to shareholder disputes. Contact one of Advent’s business valuation professionals to facilitate the bankruptcy process and, if possible, get your business back on track.

In light of the coronavirus pandemic, the American Institute of Certified Public Accountants has offered new guidelines for valuing distressed or impaired businesses. Photo by Matthew Henry from Burst

The American Institute of Certified Public Accountants has issued new guidance regarding the valuation of distressed or impaired businesses.

The guidance, which is presented as responses to frequently asked questions, distinguishes between distress, which may be a temporary condition, and impairment, which is usually permanent. The FAQs address the application of valuation adjustments and other considerations related to the coronavirus crisis.

The AICPA highlights both the perils of failing to consider the many implications of the pandemic and the risk of overcompensating for the effects of such an unprecedented event. In addition, it notes that the pandemic may have positive implications for some businesses, such as those that are able to increase market share as weaker competitors crumble.

Buyers are most interested in an acquisition target’s core competencies, and they usually prefer a clean, simple transaction. Consider buying out minority investors who could object to a deal and removing nonessential items from your balance sheet. Items that could complicate a sale include underperforming segments,nonoperating assets, andshareholder loans.

Buyers are most interested in an acquisition target’s core competencies, and they usually prefer a clean, simple transaction. Consider buying out minority investors who could object to a deal and removing nonessential items from your balance sheet. Items that could complicate a sale include underperforming segments,nonoperating assets, andshareholder loans.

Ambiguous or outdated buy-sells can cause problems when it’s time for a buyout. For example, an agreement containing undefined valuation terminology — such as “earnings” or “value” — may be subject to different interpretations.

Ambiguous or outdated buy-sells can cause problems when it’s time for a buyout. For example, an agreement containing undefined valuation terminology — such as “earnings” or “value” — may be subject to different interpretations. Business valuation is a prophecy of the future. That is, investors typically value a business based on its ability to generate future cash flow. However, with so many uncertainties in the current marketplace, forecasting expected cash flow can be challenging.

Business valuation is a prophecy of the future. That is, investors typically value a business based on its ability to generate future cash flow. However, with so many uncertainties in the current marketplace, forecasting expected cash flow can be challenging.