Advent Valuation Advisors has been named one of the Top 10 Emerging Valuation Services Companies for 2022 by CFO Tech Outlook magazine. The honorees were unveiled in the March edition of the magazine, which was dedicated to business valuation. The article is available here.

Valuing a financially troubled company requires special treatment. Photo by Andrea Piacquadio from Pexels

Over the last two years, market conditions — from cost increases and forced shutdowns to shortages of labor and supplies — have taken their toll on many businesses. While owners of distressed businesses may hope to turn things around, some will unfortunately shutter. Valuation is a prophecy of the future, not the past. So, valuing a financially troubled company requires special treatment.

Diagnosing the Situation

Valuing a distressed business is similar in many ways to valuing a healthy one: The valuation professional evaluates financial information and examines the business and its industry to assess the company’s ability to generate earnings. But troubled companies don’t behave in quite the same way as healthy companies, so valuators must approach them a little differently.

One of a valuator’s biggest challenges in valuing a struggling company is normalizing its operating results. Most valuations, even of healthy companies, involve some normalization. The valuator adjusts the company’s operating results to exclude unusual items — such as nonrecurring income or expenses. This allows the valuator to project earnings under “normal” conditions.

Determining the causes of a company’s poor performance is critical. If the company got into trouble because of poor management or excessive debt, it could have a great deal of value to a buyer with a stronger management team or greater access to capital. But if the company is struggling because of reduced demand for its products or services or because its technology has become obsolete, it may be difficult — if not impossible — to restore it to profitability.

Prescribing a Valuation Method

For healthy companies, past performance is often a reliable predictor of future success. But for troubled companies, valuations must be essentially forward-looking. The key is to identify what caused the company’s financial distress, determine whether the problem can be fixed and develop a picture of the company’s future earnings after management has turned operations around.

For this reason, valuation pros usually use income-based methods, such as discounted cash flow analysis, to value troubled companies.

Market-based methods — where valuators apply price-to-earnings multiples or other measures derived from transactions involving comparable companies — are difficult if not impossible to use. Most market data is drawn from transactions involving healthy companies, which can’t be applied to troubled companies without complex (and potentially problematic) adjustments.

The cost approach also may be particularly relevant when valuing a distressed business. While healthy companies are almost always valued as going concerns, a distressed company may be worth more in liquidation. Therefore, the valuator needs to determine its liquidation value for comparison.

Proper Treatment

Distressed companies operate under extraordinary circumstances, so different rules apply. Advent’s business valuation experts have experience working with struggling companies and can help determine what’s appropriate for your case. Contact us for more information.

Courts and experts often disagree on the applicability of marketability discounts for controlling interests. Photo by Artem Beliaikin from Pexels

In a business valuation context, the term “marketability” refers to the ability to quickly convert property to cash at minimal cost. While publicly traded stocks are readily marketable, interests in private companies typically require substantial time, cost and effort to sell. To the extent that public stock data is used to value private businesses, a discount may be warranted to reflect the lack of marketability. However, an important distinction must be made when applying these discounts to controlling interests.

Minority vs. Controlling Interests

Marketability discounts are well established when valuing minority interests in closely held businesses. Several empirical studies support and quantify these discounts. Restricted stock and pre-IPO studies, for example, demonstrate the spread between prices paid for freely traded shares and identical shares that are less marketable because they’re restricted or not yet publicly traded. Discounts typically average between 30 percent and 45 percent.

Using marketability discounts for controlling interests is controversial, although courts have sometimes accepted them. Most experts agree that the size of marketability discounts shrinks as the level of control increases. But while many argue that some amount of discount is available at all levels of control – even 100 percent – others say it is inappropriate to apply a marketability discount to a controlling interest.

Illiquidity

Marketability discounts applied to controlling interests are sometimes referred to as “illiquidity” discounts to help differentiate them from discounts taken on minority interests. With a controlling interest, it takes time and expense to complete a sale. The discount reflects the uncertainty and risk associated with the timing of the sale and the ultimate price.

The rationale underlying taking a marketability discount on a controlling interest is that fair market value is a cash equivalent concept. In contrast, a future sale of a controlling interest is speculative and expensive. The deal also may include noncash terms, such as employment contracts, restricted stock or installment payments.

For example, in a divorce case, it may seem inequitable for one spouse to receive $1 million of an illiquid business, while the other spouse receives $1 million of cash and real estate, which are considerably more liquid.

When quantifying illiquidity discounts, valuation experts consider the time, costs and risks of selling a business (or a controlling interest within it). Alternatively, they may estimate the costs of going public. No official empirical data exists to support marketability discounts on controlling interests. But all else being equal, most experts agree the discount for a controlling interest should generally be lower than for a minority interest in the same company.

Case in Point

To see how this can play out in court, let’s look at a recent divorce case where the husband’s expert applied a marketability discount on a controlling interest in the husband’s dental practice. (Kakollu v. Vadlamudi, No. 21A-DC-96, Ind. App., July 26, 2021.)

The wife’s valuation expert valued the entire practice at $3 million. The husband’s expert arrived at a value of $1.56 million after taking a 45 percent marketability discount. The lower court rejected the expert’s discount because he admitted that:

A discount greater than 35 percent would likely draw IRS attention, if it was taken in a valuation prepared for federal tax purposes,

Controlling interests may be easier to sell than minority interests,

Dental practices are easily tradeable as they have a ready market of purchasers (new dentists) graduating each year, and

The husband had no intention to sell his practice.

Because the marketability discount was the primary reason for the difference between the experts’ values, the trial court accepted the analysis prepared by the wife’s expert. The Indiana Court of Appeals upheld the decision, concluding that there was no requirement for the trial court to apply a marketability discount when determining the value of a business. You can read the decision here: https://adventvalue.com/wp-content/uploads/2022/03/Srinivasulu-Kakollu-v.-Sraina-Sowmya-Vadlamudi.pdf

Contact Us

The application and magnitude of marketability discounts are matters of professional judgment and can vary significantly from one valuation assignment to the next. The professionals at Advent Valuation Advisors can help you support or challenge the use of a marketability discount for a specific case.

With limited exceptions, events that occur after the valuation date generally are not considered in determining the value of a business interest. Photo by Wyron A on Unsplash.

The value of a business interest is valid as of a specific date. The effective date is a critical cutoff point because events that occur after that date generally are not taken into account when estimating value.

However, there are two key exceptions.

1. When an Event Is Foreseeable

Subsequent events that were reasonably foreseeable on the effective date are usually factored into a valuation. That’s because, under the definition of fair market value, hypothetical willing buyers and sellers are presumed to have reasonable knowledge of relevant facts affecting the value of a business interest. Examples of potentially relevant subsequent events are:

An offer to purchase the business,

A bankruptcy filing,

The emergence of new technology or government regulations,

A natural or human-made disaster,

A pending legal investigation or lawsuit, and

The loss of a key person or major contract.

But not all of these examples would be reasonably foreseeable. For example, you probably can’t predict when your company will be affected by a tornado or a data breach.

This issue has come to the forefront during the COVID-19 pandemic. To determine what was known or knowable about this ongoing crisis on a valuation’s effective date, experts must put themselves in the shoes of hypothetical buyers and sellers on that date and consider how they would have perceived the situation.

Many businesses have been adversely affected by the pandemic; others have taken advantage of opportunities that emerged from the the crisis. The effects also may vary depending on the company’s geographic location or industry, so valuators must evaluate the situation closely to determine what’s appropriate for the specific subject company.

In addition to facts that are publicly available, “reasonable knowledge” includes facts that a buyer would uncover over the course of private negotiations over the property’s purchase price. During normal due diligence procedures, a hypothetical buyer is expected to ask the hypothetical seller for information that’s not publicly available.

2. When a Transaction Provides an Indication of Value

A subsequent event that’s unforeseeable as of the effective date may still be considered if it provides an indication of value. However, it generally must be within a reasonable period and occur at arm’s length.

For example, in a landmark case — Estate of Jung v. Commissioner (101 T.C. 312, 1993) — the U.S. Tax Court ruled that actual sales prices received for property after the effective date may be considered when valuing a business interest, “so long as the sale occurred within a reasonable time … and no intervening events drastically changed the value of the property.” This ruling differentiates subsequent events that affect fair market value from those that provide an indication of fair market value.

Full Disclosure

When you hire a business valuation expert, it’s important to share all information that could potentially be relevant to the value of the business. This includes information about subsequent events that affect value or provide an indication of value. Once the valuation expert is aware of this information, he or she can determine whether an event is appropriate to consider when valuing the business interest.

If you require assistance with a business valuation-related matter, please contact Advent for trusted guidance.

When a business has been damaged by another party, an expert may be needed to estimate the damages. Photo by Dovis from Pexels

Financial experts are often hired to measure economic damages in contract breach, patent infringement and other tort claims. Here’s an overview of how experts quantify damages, along with some common pitfalls to avoid.

Estimating Lost Profits

Where would the plaintiff be today “but for” the defendant’s alleged wrongdoing? There are three ways experts address that question:

1. Before-and-after method. Here, the expert assumes that, if it hadn’t been for the breach or other tortious act, the company’s operating trends would have continued in pace with past performance. In other words, damages equal the difference between expected and actual performance. A similar approach quantifies damages as the difference between the company’s value before and after the alleged tort occurred.

2. Yardstick method. Using this technique, the expert benchmarks a damaged company’s performance to external sources, such as publicly traded comparables or industry guidelines. The presumption is that the company’s performance would have mimicked that of its competitors if not for the tortious act.

3. Sales projection method. Projections or forecasts of the company’s expected cash flow serve as the basis for damages under this method. Damages involving niche players and start-ups often call for the sales projection method, because they have limited operating history and few meaningful comparables.

Experts will consider the specific circumstances of the case to determine the appropriate method (or methods) for the situation.

Discounting Damages

After experts have estimated lost profits, they discount their estimates to present value. Some jurisdictions have prescribed discount rates, but, in many instances, experts subjectively build up the discount rate based on their professional opinions about risk. Small differences in the discount rate can generate large differences in valuators’ final conclusions. As a result, the discount rate is often a contentious issue.

Mitigating Factors

Another key step is to address mitigating factors. In other words, what could the damaged party have done to minimize its loss?

For example:

• A manufacturer that suffers a business interruption should minimize the impact by resuming operations at a temporary location or outsourcing production to another company, if possible.

• A wrongfully terminated employee needs to make a reasonable effort to find another job.

• An antitrust plaintiff prevented from entering a particular market should explore opportunities to invest in alternative markets.

• A plaintiff in a breach-of-contract case should make a reasonable effort to replace the business lost as a result of the defendant’s wrongdoing.

Most jurisdictions hold plaintiffs at least partially responsible for mitigating their own damages. Similar to discount rates, this subjective adjustment often triggers widely divergent opinions among the parties involved.

Avoiding Potential Pitfalls

Some key factors need to be considered to avoid over- or underestimating a plaintiff’s loss. For example, the taxation of damages can have a significant impact on an expert’s conclusion. If the plaintiff must pay taxes, an after-tax assessment wouldn’t be equitable. Also realize that some parts of a damages award, such as return of capital, may be nontaxable and require an after-tax estimate.

Taxes also need to be handled properly when lost profits are discounted to present value. In other words, if damages need to be calculated on a pretax basis, the expert should use pretax discount rates. Mismatching after-tax discount rates to pretax cash flows would overstate damages, all else being equal.

In addition, it’s important to not assume that damages will occur into perpetuity. Economic damages generally occur over a finite period. They have a beginning and an end. Eventually most plaintiffs can overcome the effects of the defendant’s alleged wrongdoing.

For More Information

When calculating economic damages, there isn’t a one-size-fits-all approach. What’s right depends on the facts of your particular case. Contact the experts at Advent Valuation Advisors to develop an estimate that avoids potential pitfalls and can withstand scrutiny in court.

A married person filing jointly may be held responsible if a spouse cheats on their tax return. Photo by Burak Kostak from Pexels

When you got married, you knew it was for “better or worse.” But you might not know about laws that hold you responsible if your spouse cheats on a tax return.

Married couples filing jointly should be aware that:

You are both responsible for tax, interest and penalties — even after a divorce or the death of a spouse.

The IRS may hold you responsible for all the tax due even if there is a divorce decree stating that your ex-spouse is accountable for previous joint returns.

You can be liable for tax even if none of the income on a tax return is attributed to you.

To illustrate how the law works, let’s say you have a wage-earning job and your spouse is self-employed. You file joint tax returns. Next year, you get divorced and a year later, the IRS audits your tax return. Your ex-spouse is nowhere to be found, and auditors determine that he or she didn’t report all the income from the business.

What Could Happen?

You are generally liable for paying the tax due, plus interest and any penalties. Your wages can be seized by the IRS even if you paid every penny owed on your share of the family income.

Fortunately, there may be a way to get off the hook. In some situations, the tax law provides “innocent spouse” relief if you can prove:

There is a substantial understatement of tax attributable to the grossly erroneous items of your spouse or ex-spouse.

The hidden income belonged to your ex-spouse and you didn’t benefit from it.

You didn’t know or have reason to know about the understatement.

It would be inequitable to hold you liable.

In January 2012, the IRS released proposed streamlined procedures that make it easier to obtain equitable relief. The new guidelines also include an exception to the requirement that items must be attributable to the ex-spouse when that spouse’s fraud is the cause of the understatement or deficiency.

Be aware that the IRS is required to notify an ex-spouse that relief has been requested so that he or she can elect to participate. There are no exceptions, even for victims of domestic violence.

“Innocent” versus “Injured” Spouse

If your current or former spouse has gotten you into tax trouble, you may be able to get help from the IRS. It all depends on whether the tax agency considers you “injured” or “innocent.” You probably think you qualify as both, but they are two different legal terms:

An injured spouse files a joint return and loses all or part of a refund because of a spouse’s debts.

An innocent spouse claims no liability for items on a joint tax return that belong to a spouse or ex-spouse. Let’s say you and your current spouse file a joint tax return and are expecting a large refund. But you receive a notice from the IRS stating that your refund is being seized to pay a debt owed only by your spouse. For example, back taxes from before you married, past due child support, a delinquent student loan or other federal debt.

You may be able to recover your portion of a joint tax refund that the IRS seized. To qualify, you must have earned your own income and made your own federal tax payments. Ask your tax advisor for more information if you think you qualify.

Advice: Don’t count on innocent spouse relief if you know your spouse is cheating on tax returns. The IRS often denies relief. Consider filing separate tax returns — especially if you’re in the process of a divorce. It may save you a bundle in the future. For more information about your situation, consult with your tax advisor.

If you require the valuation of a business, calculation of reasonable compensation or forensic assistance in a matrimonial matter, please contact Advent Valuation Advisorsfor trusted guidance.

The U.S. Tax Court recently ruled that payments made to a corporate taxpayer’s three shareholders were dividends — not compensation for personal services rendered. The court’s reasoning also may be relevant in shareholder disputes and divorce cases when the parties disagree about whether compensation should be deducted from earnings when valuing a business interest. (Aspro, Inc. v. Commissioner, T.C. Memo 2021-8, Jan. 21, 2021.)

Background

Under current tax law, a corporation may deduct all ordinary and necessary expenses paid or incurred during the tax year in carrying on any trade or business, including a reasonable allowance for salaries or other compensation for personal services rendered. In the case of compensation payments, a test of deductibility is whether they’re in fact payments purely for services.

On the other hand, distributions to shareholders disguised as compensation aren’t deductible for federal income tax purposes. Specifically, Internal Revenue Code Section 162 says:

Any amount paid in the form of compensation, but not in fact as the purchase price of services, is not deductible. An ostensible salary paid by a corporation may be a distribution of a dividend on stock. This is likely to occur in the case of a corporation having few shareholders, practically all of whom draw salaries. If in such a case the salaries are in excess of those ordinarily paid for similar services and the excessive payments correspond or bear a close relationship to the stockholdings of the officers or employees, it would seem likely that the salaries are not paid wholly for services rendered, but that the excessive payments are a distribution of earnings upon the stock.

Case Facts

The taxpayer operated as an asphalt paving business. Most of its revenue came from contracts with government entities. These public projects are awarded to the low bidder. Aspro has three owners:

Shareholder A is an individual who owned 20% of the company,

Shareholder B is a corporation that owned 40% of the company, and

Shareholder C is a corporation that owned 40% of the company.

Shareholder A also served as the company’s president and was responsible for its day-to-day management. His responsibilities included bidding on projects. Shareholder A often spoke to the individuals who owned corporate shareholders B and C to get their advice on bidding for projects.

In 2014, Aspro paid management fees to its shareholders for their advisory services on how to bid for projects. Aspro then deducted these management fees for personal services rendered. Neither in 2014 nor in any prior year did Aspro pay dividends to its shareholders. The IRS denied the deduction, claiming the fees were actually dividends.

Tax Court Decision

The Tax Court agreed with the IRS. It didn’t dispute that a portion of payments made to Shareholder A potentially might have been compensation for personal services. However, since the payments weren’t purely compensation, they weren’t deductible for federal income tax purposes.

Factors underlying the court’s decision to classify the payments as dividends, not a form of compensation, include:

Lack of historical dividend payments. Aspro is a corporation with few shareholders that never distributed any dividends during its entire corporate history; it merely paid management fees.

Payments corresponding to ownership percentages. The management fees weren’t exactly pro rata among the three shareholders. However, the two corporate shareholders always got equal amounts, and the percentages of management fees all three shareholders received roughly corresponded to their respective ownership interests.

Payments to shareholders, not individuals. Aspro paid the amounts to corporate shareholders B and C, instead of to the individuals who actually performed the advisory services.

Timing. Aspro paid management fees as lump sums at yearend, rather than paying them throughout the year as the services were performed.

Lessons Learned

The appropriate treatment of payments to shareholders should be decided on a case-by-case basis. The decision has implications beyond federal income taxes. To the extent that a company’s value is based on its earnings or net free cash flow — say, under the income or market approaches — the deductibility of these payments can have a major impact on the value of a business interest.

The federal income tax rules for how to treat these expenses can provide objective guidance when classifying payments for other purposes. In some cases, it may be appropriate to adjust a company’s earnings for deductions that represent dividends, based on the facts of the case.

For more information about the classification of compensation and dividends or other valuation issues, please contact the professionals at Advent Valuation Advisors

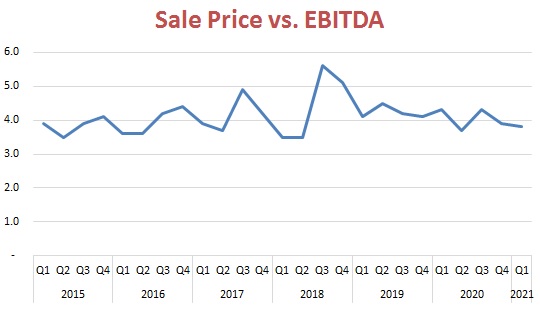

The median price-to-EBITDA multiple among deals reported to DealStats fell slightly to 3.8 during the first quarter of 2021, down from 3.9 in the fourth quarter of 2020, suggesting transaction prices remain under pressure from the coronavirus pandemic.

According to the latest edition of DealStats Value Index, the four-quarter average EBITDA (earnings before interest, taxes, depreciation and amortization) multiple for the year ending in March 2021 was 3.9, the lowest such average since the period ending in the third quarter of 2016.

EBITDA measured as a percentage of net sales fell to 10 percent in the first quarter of 2020, due at least in part the ongoing economic toll of the pandemic and resulting restrictions. The reduction also reflects a longer-term trend of lower margins. EBITDA margins for transacted businesses have fluctuated between roughly 10.5 percent and 12 percent since late 2018, according to DealStats. From 2015 to 2018, they generally moved between 11 percent and 14.5 percent. DealStats does not indicate if the EBITDA margin metric is a median or an average.

Transaction reporting appears to have slowed with the pandemic. Of 15 sectors tracked by DealStats, just three met the minimum of 10 reported transactions during the first quarter required for the inclusion of sector-specific multiples.

DealStats is a database of private-company transactions maintained by Business Valuation Resources. The database is used by business appraisers when applying the market approach to valuation. Multiples such as sale price-to-EBITDA can be derived from transactions involving similar businesses and used to estimate the value of a company, subject to adjustments for unique characteristics of the business being valued.

William Quackenbush, director of Advent Valuation Advisors, has been elected into the College of Fellows of the American Society of Appraisers and awarded the coveted Fellow Accredited Senior Appraiser (FASA) designation. Fellowship is the highest honor bestowed by the Society on a member and recognizes the professionalism and invaluable contributions the member has made.

Earning the FASA makes Bill one of a small, select group of members that currently hold this honor. A member since 1998, he had previously been designated as an Accredited Senior Appraiser (ASA) within the business valuation discipline of the Society.

“Your exemplary service and dedication have helped ASA maintain its position of leadership among professional appraisal organizations around the world,” said Lorrie Beaumont, ASA, International President of the American Society of Appraisers. “Your commitment to excellence in your practice and in every task you have undertaken on behalf of the Society has contributed to the advancement of the valuation profession in the minds of those who use, practice and regulate appraisal services.”

Bill is the founder and current director of Advent Valuation Advisors, a national business valuation and financial advisory services firm with offices in Newburgh, Poughkeepsie and Manhattan. He has been a contributing author or technical reviewer of several books on business valuation and business valuation-related topics and has been a frequent speaker on business valuation-related issues to professional associations.

“The team at Advent is thrilled to see Bill honored for his exceptional and wide-ranging contributions to the business valuation profession,” said Lorraine Barton, Partner of Advent Valuation Advisors. “This prestigious designation recognizes Bill’s years of dedication to his craft, his clients and his colleagues.”

Bill has served as the Chair of the Business Valuation Committee (BVC) of the American Society of Appraisers and many functional committees of the organization. He has been a course developer and is currently an instructor and Vice Chair of the Board of Examiners. He has taught business valuation internationally and for the Big Four accounting firms for over 15 years.

Bill remarked, “The American Society of Appraisers has been the leader in the advancement of the business valuation profession. My work with the Society has been and continues to be immensely rewarding. I am honored to have been elected into the College of Fellows and to join those who have contributed so much to the profession.”

There are many factors to consider when determining reasonable owners’ compensation. Photo by Matthew Henry from Burst

For most privately held businesses, owners’ compensation is one of the largest expenses on the income statement, especially when all the related perks and hidden costs are calculated. Compensation should accurately reflect what others would receive for similar duties in a similar setting. Reasonable compensation levels are important not only for state and federal tax purposes, but also to get an accurate estimate of the fair market value of the business.

Total Compensation Package

Before compensation can be assessed as reasonable, all components of the package must be calculated, including:

Direct salaries, bonuses and commissions,

Stock options and contingent payments,

Payouts under golden parachute clauses,

Shareholder loans with low (or no) interest and other favorable terms,

Company-owned or leased vehicles and vehicle allowances,

Moving and relocation expenses,

Subsidized housing and educational reimbursements,

Excessive life insurance or disability payments, and

Other perks, such as cafeteria plans, athletic club dues, vacations and discounted services or products.

In addition, owners’ compensation may be buried in such accounts as management and consulting fees, rent expense and noncompete covenants.

IRS Guidance

The IRS has published a guide titled, “Reasonable Compensation: Job Aid for IRS Professionals.” IRS field agents use this guide when conducting audits to help determine what’s reasonable and how to estimate an owner’s total compensation package.

The IRS is on the lookout for C corporations that pay employee-shareholders excessive salaries in place of dividends. This tactic lowers the overall taxes paid, because salaries are a tax-deductible expense and dividends aren’t.

Owner-employees of C corporations pay income tax on salaries at the personal level, but dividends are subject to double taxation (at the corporate level and at each owner’s personal tax rate). If the IRS decides that a C corporation is overpaying owners, it may reclassify part of their salaries as dividends.

For S corporations, partnerships and other pass-through entities, the IRS looks for businesses that underpay owners’ salaries to minimize state and federal payroll taxes. Rather than pay salaries, S corps are more likely to pay distributions to owners. That’s because distributions are generally tax-fee to the extent that the owner has a positive tax basis in the company.

The IRS job aid lists several sources of objective data that can be used to support compensation levels, including:

General industry surveys by Standard Industry Code (SIC) or North American Industry Classification Systems (NAICS),

Salary surveys published by trade groups or industry analysts,

Proxy statements and annual reports of public companies, and

Private company compensation reports such as data published by Willis Towers Watson, Dun & Bradstreet, the Risk Management Association or the Economic Research Institute.

“Reasonable and true compensation is only such amount as would ordinarily be paid for like services by like enterprises under like circumstances,” states the IRS job aid.

Compensation Benchmarks

Beyond IRS audits, the issue of reasonable compensation may become an issue in shareholder disputes, marital dissolutions and other litigation matters. When valuing a business for these purposes, a company’s income statement may need to be adjusted for owners’ compensation that is above or below market rates.

Courts often rely on market data to support owners’ compensation assessments. But it can be a challenge to find comparable companies — and comparable employees within those companies. The five areas that courts consider when evaluating reasonable compensation are:

The individual’s role in the company,

External comparisons of the salary with amounts paid to similar individuals in similar roles,

Character and condition of the company,

Potential conflicts of interest between the individual and the company, and

Internal inconsistency in the way employees are treated within the organization.

Owners can control compensation, and that creates an inherent conflict of interest when estimating what’s reasonable. External comparisons are key to supporting compensation levels. Business valuation experts typically interview owners to get a clearer picture of their experience, duties, knowledge and responsibilities.

Get It Right

For more information about reasonable owners’ compensation, please contact the business valuation professionals at Advent Valuation Advisors. We can help estimate total compensation levels, find objective market data and adjust deductions that are above or below market rates.

Over the last two years, market conditions — from cost increases and forced shutdowns to shortages of labor and supplies — have taken their toll on many businesses. While owners of distressed businesses may hope to turn things around, some will unfortunately shutter. Valuation is a prophecy of the future, not the past. So, valuing a financially troubled company requires special treatment.

Over the last two years, market conditions — from cost increases and forced shutdowns to shortages of labor and supplies — have taken their toll on many businesses. While owners of distressed businesses may hope to turn things around, some will unfortunately shutter. Valuation is a prophecy of the future, not the past. So, valuing a financially troubled company requires special treatment.

The value of a business interest is valid as of a specific date. The effective date is a critical cutoff point because events that occur after that date generally are not taken into account when estimating value.

The value of a business interest is valid as of a specific date. The effective date is a critical cutoff point because events that occur after that date generally are not taken into account when estimating value.

Where would the plaintiff be today “but for” the defendant’s alleged wrongdoing? There are three ways experts address that question:

Where would the plaintiff be today “but for” the defendant’s alleged wrongdoing? There are three ways experts address that question:

You are generally liable for paying the tax due, plus interest and any penalties. Your wages can be seized by the IRS even if you paid every penny owed on your share of the family income.

You are generally liable for paying the tax due, plus interest and any penalties. Your wages can be seized by the IRS even if you paid every penny owed on your share of the family income.

Under current tax law, a corporation may deduct all ordinary and necessary expenses paid or incurred during the tax year in carrying on any trade or business, including a reasonable allowance for salaries or other compensation for personal services rendered. In the case of compensation payments, a test of deductibility is whether they’re in fact payments purely for services.

Under current tax law, a corporation may deduct all ordinary and necessary expenses paid or incurred during the tax year in carrying on any trade or business, including a reasonable allowance for salaries or other compensation for personal services rendered. In the case of compensation payments, a test of deductibility is whether they’re in fact payments purely for services.