Ever wonder why a startup company that hasn’t turned a profit and may not even have a clear path to generating one can command a billion-dollar valuation?

What drives the value of these unicorns? Why are early investors so eager to pour money into them? Antonella Puca talks about the challenges of unicorn valuation and the importance of intangibles at aicpa.org.

Business Brokers Note Dip in Seller Confidence in First Quarter

Seller sentiment declined during the first quarter in four out of five price segments below $50 million, according to a survey of business brokers and M&A advisors. Photo by rawpixel.com from Pexels

It’s still a seller’s market, but the balance of power in business transactions has begun to shift, according to the latest edition of Market Pulse, the quarterly survey of business brokers conducted by the International Business Brokers Association and M&A Source.

The national survey is intended to capture market conditions for businesses being sold for less than $50 million. It divides that market between Main Street businesses with values of $2 million or less, and lower middle-market ones in the $2 million to $50 million range.

The report for the first quarter of 2019 describes a robust market in which sellers of businesses hold the advantage in all segments except the smallest (under $500,000). But it also notes that seller confidence declined over the preceding year across all market segments except for the $5 million to $50 million value range.

A seller’s market is reflected in seller confidence in excess of 50 percent.“Although it is still a strong seller’s market with strong values, this is the first time in years that we’ve seen four out of five sectors report a dip in seller market sentiment,” said Craig Everett, PhD, who is quoted in the report. Everett is director of the Pepperdine Graziadio Business School’s Private Capital Markets Project, which compiled the survey’s results. “This is a sign the market has peaked, and more people are expecting a correction in the year or two ahead.”

The first-quarter survey of 292 business brokers and M&A advisors was conducted from April 1-15.

Other takeaways from the report include:

Larger companies are selling at higher multiples than smaller ones. During the first quarter, sales for less than $500,000 carried a median multiple of price to seller’s discretionary earnings of 2.0. Businesses in the $1 million to $2 million range sold for three times SDE. The median EBITDA multiple paid for businesses in the $2 million to $5 million range was 4.3, compared to the median multiple of 6.0 for businesses in the $5 million to $50 million range.

Larger companies tend to sell for a greater percentage of asking price. Lower middle-market companies ($5 million to $50 million in value) sold for 101 percent of the asking price or internal benchmark. Small Main Street companies (less than $500,000) sold for 85 percent of asking price.

One reason for the difference: Larger companies are more likely to attract interest from private equity or synergistic buyers, according to David Ryan of Upton Financial Group, who is cited in the report.

Smaller businesses also tend to depend more heavily on their owners, which means more value is lost when the owner leaves the business. For more information on the report, go to: https://www.ibba.org/market-pulse

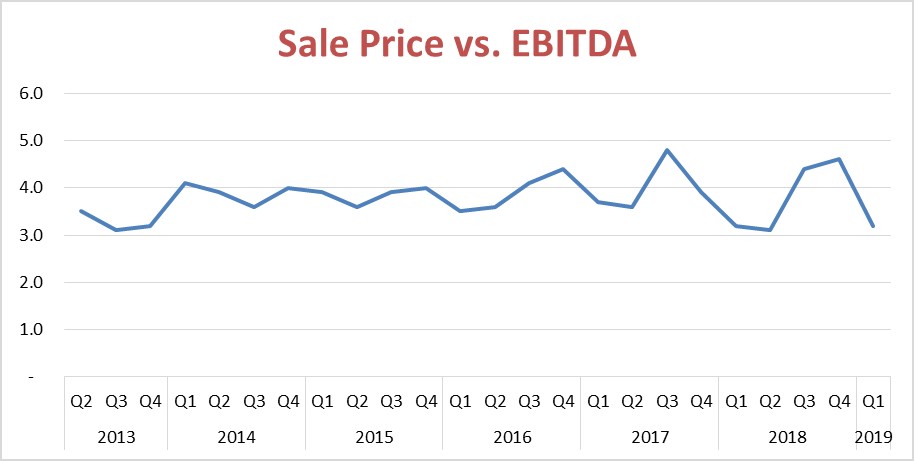

The relationship between EBITDA and sale price for private business transactions has grown more volatile over the past two years, according to the DealStats Value Index data for the first three months of 2019. Source: DealStats Value Index, 2Q 2019

Bargain shoppers took center stage during the first three months of the year, as EBITDA multiples for sales of private businesses dropped sharply, according to the latest edition of the DealStats Value Index.

The ratio of median selling price to EBITDA (earnings before interest, taxation, depreciation and amortization) fell during the first quarter to 3.2, from 4.6 during the final three months of 2018. It was the lowest level reported since the second quarter of 2018, when the median multiple hit a five-year low of 3.1.

DealStats is a database of private-company transactions maintained by Business Valuation Resources. Those transactions are used by business appraisers when applying the market approach to valuation. Multiples such as sale price-to-EBITDA can be derived from transactions involving similar businesses and used to estimate the value of a company.

Business appraisers use ratios such as price-to-EBITDA in roughly the same manner that home appraisers use price-per-square-foot – to create a ballpark estimate of value, subject to adjustments for unique features of the entity being valued.

Other popular ratios are price-to-sales, price-to-EBIT (earnings before interest and taxes, aka operating profit) and price-to-discretionary earnings. We could spend a full column discussing that last one; for now, think of it as the total benefits available to the business owner.

Rising margins

While the sale price-to-EBITDA multiple declined during the first quarter, another measure tracked by DealStats increased. EBITDA margin – the percentage of revenue represented by EBITDA – rose to 15 percent during the first quarter of 2019, up from 11 percent in the previous quarter. EBITDA margin and the sale price-to-EBITDA ratio tend to move in opposite directions.

In short, companies sold during the first three months of the year were more profitable (as measured by EBITDA) than those sold in the previous half-year, but sold at lower multiples of that enhanced profit level.

Increased volatility

The relationship between selling prices and EBITDA has grown more volatile over the past two years, after moving in a more narrow range from 2014 to mid-2017, according to the DealStats Value Index.

What is driving this increased volatility? Answering that is a little like trying to explain the stock market’s roller-coaster ride of the past year. If we could divine satisfactory solutions to these riddles, we’d be in a different line of work, perhaps reading Tarot cards or playing the ponies.

One factor that can create the appearance of volatility is a shift in the mix of businesses that sell from one quarter to the next. Companies in different industries tend to sell for distinct multiples. The ratio of sale price-to-EBITDA for finance and insurance companies, for instance, was 7.5 during the quarter, according to BVR, while the multiple for retail trade was 3.8. If a wave of consolidation hits retailers, it could skew the overall multiples without implying anything regarding the appropriate multiples for any given industry or business.

Think of it this way: If a developer came to town and built a few dozen pricey Colonials over a year or two, the median sale price for homes in your town might increase substantially. That would not necessarily mean that your humble split-level with its well-manicured lawn and partially obstructed mountain views had increased in value proportionately.

It remains to be seen if the recent drop in the EBITDA multiple and spike in volatility are temporary blips or signals of more sustained change. Stay tuned.

A recent District Court decision has implications for the use of tax-affecting in the valuation of S corporations. Photo by Sarah Pflug from Burst

Lorraine Barton Advent Valuation Advisors

On March 25, 2019, the U.S. District Court – Eastern District of Wisconsin issued an important decision supporting the use of tax-affecting in valuing pass-through entities. In Kress v. United States, Chief Judge William C. Griesbach relied heavily on the taxpayer’s expert in valuing non-controlling interests in a Subchapter S operating company called Green Bay Packaging, Inc. (“GBP”).

In the taxpayer’s expert report, GBP was first valued as a C-corporation equivalent, which included tax–affecting. Next, quantitative and qualitative adjustments were made to address economic benefits attributed to the Subchapter S election.

The valuation community and taxpayers have been fighting the IRS over this issue for years, starting with Gross v. Commissioner (TCM 1999-254) in 1999, which rejected the use of tax-affecting when valuing pass-through entities. Courts have generally sided with the IRS in opposing the tax-affecting of pass-through entities in subsequent cases such as Estate of Gallagher v. Commissioner (TCM 2011-148) in 2011.

In Kress v. United States of America (Case No. 16-C-795, U.S. District Court, Eastern District of Wisconsin), plaintiffs James and Julie Ann Kress sued to recover an overpayment of gift taxes. The court accepted the taxpayer’s valuation report, in which GBP was tax-affected as a C corporation, supporting the point that valuation experts have been arguing for several years. While the District Court’s decision in Kress does not carry the precedential weight of a U.S. Tax Court decision, it should be valuable to other courts considering the issue.

In his report, the taxpayer’s appraiser tax-affected the earnings of the S corporation in appraisals filed as of December 31, 2006, 2007 and 2008. The court accepted the fair market value as filed by the taxpayer, with only minor adjustments to the applied discounts for lack of marketability (DLOM).

In their respective reports, the IRS’s appraiser and the taxpayer’s expert each tax-affected GBP’s S corporation earnings as if it were a C corporation. This is significant, because the IRS has held the position in recent years that earnings of pass-through entities (S corporations, LLCs and partnerships) should not be tax-affected, because they do not pay entity-level taxes. Business appraisers have generally endorsed the practice of tax-affecting pass-through entities, arguing that the tax benefit of pass-throughs should be based on the effective difference in the after-tax income of their owners.

In the Kress case, this was not an issue, as both appraisers tax-affected GBP’s earnings. The IRS’s expert also applied a pass-through benefit in its application of the income approach, while the taxpayer’s expert did not.

After acknowledging the efficacy of tax-affecting, the court went even further, stating, “The court finds GBP’s subchapter S status is a neutral consideration with respect to the valuation of its stock. Notwithstanding the tax advantages associated with subchapter S status, there are also noted disadvantages, including the limited ability to reinvest in the company and the limited access to credit markets. It is therefore unclear if a minority shareholder enjoys those benefits.”

In its decision, the court did not accept the S-corporation premium (pass-through benefit) put forth by the IRS’s valuation expert, resulting in a nearly complete victory for the taxpayer. The decision represents an important point of inflection in the controversy over the tax-affecting of pass-through entities and the application of a premium for pass-through entity status.

Over the past 20 years, the application of a premium to pass-through entities based on their pass-through tax status has been a heavily debated topic. In the Kress case, such a premium was not applied by the court. While not all concur, we believe that today, most valuation experts have concluded that pass-through entities may deserve a premium when compared to otherwise identical C corporations.

It is worth noting that the gifts in the Kress case were from 2006, 2007 and 2008, prior to the pass-through tax benefit gaining full traction in the debate within the valuation community. It will be interesting to see if prevailing thought and application change in the future.

Kress will clearly be an important reference for taxpayers in gift- and estate-tax appraisal cases where the IRS argues against tax-affecting of S corporation earnings and for a premium in the valuation of pass-through entities relative to otherwise identical C corporations. The case should be considered as support for tax-affecting the earnings of a company organized as a pass-through entity for income tax purposes.

Lorraine Barton is a partner with Advent Valuation Advisors. She can be reached at lbarton@adventvalue.com.

Advent Valuation Advisors, LLC, takes great pleasure in announcing that Lorraine Barton, CPA/ABV/CFF, CIRA, CVA, MAFF, MBA, has been admitted to the partnership.

Lorraine joined Advent, an affiliate of accounting and advisory firm RBT CPAs, LLP, in 2015. She has an extensive and varied accounting, valuation and litigation-support background in private industry and public accounting.

Lorraine has provided bankruptcy-support services since 2002 and business valuation services since 2004. She previously served as interim chief financial officer of a $125 million credit card processing company operating in Chapter 11 bankruptcy, helping to facilitate the sale of the business and saving more than 100 jobs.

At Advent, she and her team provide valuation and litigation-support services to closely held businesses and their advisors for purposes including mergers and acquisitions, buy-sell agreements, divorce, estate and gift-tax planning and corporate reorganizations.

Lorraine has completed a 40-hour divorce mediation training program that meets the requirements of the New York Association of Collaborative Professionals. She and the firm have wide-ranging experience in matrimonial finance, including asset tracing, lifestyle analysis and forensic examination.

Lorraine lives in Fishkill and has two sons. She is a graduate of Leadership Orange and serves on the NYSSCPA Business Valuation Committee.

She is also a member of the American Institute of Certified Public Accountants (AICPA), the National Association of Certified Valuators and Analysts (NACVA), the Association of Insolvency and Restructuring Advisors (AIRA) and the Hudson Valley Collaborative Divorce & Dispute Resolution Association (HVCDDRA).

“We are so pleased to welcome Lorraine as the newest partner in Advent Valuation Advisors,” said Michael Turturro, managing partner of RBT CPAs. “Lorraine is a crucial part of our continued growth. I wish her congratulations and many years of continued success!”